Duolingo: The Owl Has a Distribution Problem

$DUOL Q1 2026 ER Update

Duolingo is probably the best consumer education product in the world.

I still believe that.

The app is getting better. Speaking practice is becoming more central. AI is helping them create content at a speed that would have been impossible a few years ago. The long-term thesis, in my view, is still the same: Duolingo is not just a language app. It is trying to become the learning ontology. The place where AI is not just a chatbot, but a teacher.

That was the core of my last $DUOL update: Duolingo’s AI Pivot: The Teacher Model Thesis.

But Q1 2026 also exposed the other side of the story.

Duolingo is becoming a better teacher, but it may have a problem finding enough new students.

And for a company valued on years of user growth, that matters.

Q1 2026: good numbers, but the mix matters

The headline numbers are not bad.

In Q1 2026, Duolingo reported:

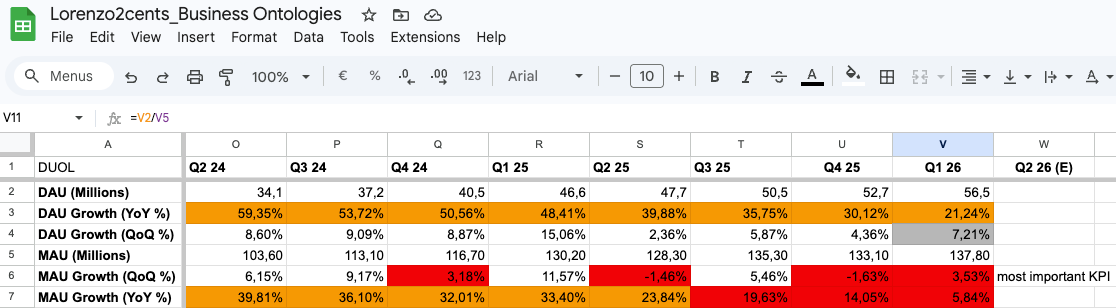

DAUs of 56.5 million, up 21% YoY.

MAUs of 137.8 million, up only 6% YoY.

Paid subscribers of 12.5 million, up 21% YoY.

Revenue of $292.0 million, up 27% YoY.

Total bookings of $308.5 million, up 14% YoY.

Free cash flow of $147.8 million, a 50.6% FCF margin.

So this is not a broken business.

Actually, the opposite. Duolingo is still growing revenue at 27%, printing free cash flow, and improving monetization. Paid subscriber penetration increased to 9.4% from 8,9% in Q1 2025 and 9,3% in Q4 2025.

The company is clearly getting better at farming the existing base.

The problem is the top of the funnel.

MAUs grew only 6% YoY and 3,5% QoQ, while DAUs grew 21% YoY and 7% QoQ.

Being MAU a leading indicator for DAU, and being the former in deceleration, the latter will likely follow soon.

That means engagement is improving, but the pool of users is not expanding nearly as fast as before.

DAU/MAU went from 35.8% to 41.0% YoY.

That is impressive product execution.

But it also tells you where the growth is coming from: retention, habit, conversion, monetization.

Not enough from new user acquisition.

The bull case is still alive: AI is making Duolingo a better product

The best part of the quarter was product velocity.

Duolingo is attacking the biggest weakness of the app: speaking.

Management wrote in the shareholder letter:

Speaking practice, historically the biggest gap for learners on Duolingo, is now a core part of the product.

They added that Video Call remains one of their most impactful paid features and that, over the last year, they have “more than doubled the average number of words spoken per user in Video Call.”

This matters because Duolingo’s historical weakness was obvious.

It was great at making you show up every day. It was great at teaching vocabulary and grammar in small chunks. It was not great at making you speak.

That gap is now closing.

They introduced spoken tokens, flashcards, and Speaking Adventures. Management described spoken tokens as a change that “enables almost every exercise in Duolingo to become speaking practice.”

This is exactly what I want to see.

If Duolingo becomes the place where a beginner can go from zero to real conversation, the product becomes much more valuable. Not because it adds another feature, but because it moves closer to the real job to be done: teach me until I can actually use the language.

AI is also changing the content creation curve.

This was the strongest quote of the quarter:

In Q1 2026 alone, we published 20,500 course units across our language courses, up from 7,100 per quarter in 2025 and 1,800 per quarter in 2024.

Management added that automating more of the content creation process lets them push changes across many courses at once and improve quality faster.

This is the AI tailwind.

Most consumer AI stories are vague. Duolingo’s is very concrete: more content, faster iteration, more speaking, more personalization, lower content bottlenecks.

This supports my teacher model thesis.

A generic LLM can translate, explain grammar, or roleplay a conversation. But Duolingo has the structured curriculum, the user behavior data, the retention loops, the A/B testing engine, and the feedback loop on what actually helps people learn.

In my view, that is the moat.

The raw model is not the product. The learning system around the model is the product.

But the funnel is the problem

Here is the part I do not like.

On the call, they were asked directly about MAU growth and top of funnel. Luis von Ahn answered:

The reality is that top of funnel has been about flat for certainly for this quarter, and we would like to accelerate it.

He then explained that the historical growth driver has been word of mouth:

Again, the main thing that has been responsible for top of funnel historically has been word-of-mouth. And word-of-mouth is this interesting thing that is beautiful because it is free, but we do not have that much control over it in terms of being able to measure it the same way that we can measure retention.

That is the key issue.

Duolingo has world-class retention mechanics. They can measure them. They can A/B test them. They can improve them.

But the main top-of-funnel engine is word of mouth, and management openly admits they do not have the same level of control there.

The Google Trends screenshot makes the same point visually.

Duolingo reached peak search interest last year around the Dead Duo campaign. That campaign was genius: almost free, impossible to ignore, and very Duolingo. But that is exactly the point. You cannot schedule virality every quarter.

After Dead Duo, interest did not keep compounding. It got worse. That does not mean the brand is dead. It means word of mouth is not a controllable machine. It is a powerful engine when it works, but it is not the same as paid distribution, network effects, or owned social graphs.

This is not fatal.

But it is a different type of risk.

If MAU growth keeps slowing, DAU growth will eventually follow. DAU/MAU cannot expand forever. At some point, the ratio saturates. When that happens, the business needs new users again.

This is why I am more cautious after Q1.

The market is not wrong to ask whether Duolingo’s growth is structurally slowing. The question is whether this is a temporary transition year, while management invests in teaching better and user growth, or whether the core organic acquisition engine is reaching saturation in the most mature markets.

The D2C lesson: distribution is everything

The more I follow companies like Duolingo, Oddity, Hims and Lemonade, the more I think the same lesson keeps coming back.

D2C is brutally hard.

When it works, it looks magical. You own the customer. You own the data. You own the product loop. You can compound without paying rent to a platform forever.

But distribution is still the bottleneck.

Meta sits on a goldmine because it owns attention and distribution. Most D2C companies have to fight for it every day.

Duolingo’s advantage was that it escaped the usual D2C trap. It did not need to spend heavily on performance marketing because the product itself created word of mouth. The owl became the distribution channel.

That was a superpower.

Now it may also be the constraint.

Luis was very honest about performance marketing:

Performance marketing at Duolingo has been this interesting thing that because our free version is so good, it has not been easy for us to do profitable performance marketing because what happens is we acquire people and then they are super happy as free users.

He added:

At the moment, in some geographies, we have profitable performance marketing, but in many geographies, we do not.

This is almost an Innovator’s Dilemma.

Duolingo’s free tier is the reason the company became huge. It creates trust, habit, brand love, and scale. But the same free tier makes paid acquisition harder because many acquired users land in the free product and stay there.

If they make the free tier worse, they damage the product and the brand.

If they keep it too good, performance marketing ROI is limited.

So the business has to thread a very narrow needle: keep the free product excellent enough to drive word of mouth, while making the paid product valuable enough to justify acquisition spend.

That is not easy.

Asia and China may be the answer

There is one important counterpoint.

The problem is not equally bad everywhere.

Luis said Asia is the fastest-growing region, and China is particularly interesting. On the call, he said:

One of the things that is interesting about Asia is in a number of large Asian markets we can do profitable performance marketing

He also said: “We are able to acquire profitably” in China, where the users are English learners.

That matters.

If Duolingo can use performance marketing profitably in underpenetrated Asian markets, then the top-of-funnel issue may be more of a mature-market problem than a global problem.

The China brand partnerships are also interesting.

Luis mentioned Luckin Coffee and a coming McDonald’s China partnership, and said:

We have had incredible brand partnerships in China.

But he also made the more important point:

China is not just growing fast because of the great partnerships. I think it is kind of the other way around. I think the great partnerships are coming in part because we are growing fast and because we are seen as a very cool brand.

This is the bull version of the story.

Duolingo may not need to solve paid acquisition everywhere. It may need to professionalize it where it works, use partnerships where the brand has pull, and keep improving the product so word of mouth reaccelerates.

That is possible.

But it is not yet proven.

The other answer: make learning multiplayer

There is another path I would like to see more aggressively.

Duolingo should take the chess playbook and apply it to languages, math, music, and every course where it makes sense.

In Q3 2025, management wrote that chess had become Duolingo’s fastest-growing subject. In the same shareholder letter, Luis also said they had introduced player-vs-player on the chess course.

That is the most interesting user acquisition clue, in my view.

Multiplayer changes the growth equation.

A solo lesson is retention.

A multiplayer lesson can become distribution.

If I challenge a friend to a chess puzzle, a vocabulary duel, a speaking battle, a grammar race, or a math challenge, I am not just using the product. I am pulling someone else into the product.

That is how word of mouth becomes less random.

Today, Duolingo’s social graph is still relatively weak compared to what it could be. Streaks, leagues and leaderboards are powerful, but they mostly make the individual user come back. Multiplayer can make users bring other users back.

This is where the product can create its own acquisition loop.

Imagine language learning with real-time speaking battles. One user learning Spanish, another learning English. Short, structured, gamified conversations where both users improve and both users have a reason to invite friends.

That would be much closer to a true learning network.

And it fits Duolingo perfectly because the company already knows how to make hard things feel like a game.

The 2026 strategy sounds like “improve the product and pray”

I am exaggerating a little, but not much.

Management’s strategy for user growth is basically:

Teach better.

Improve speaking.

Make the free tier more engaging.

Invest more in marketing, especially in underpenetrated regions.

Hope better learning outcomes create more word of mouth.

This can work.

Actually, it is probably the right strategy for a product like Duolingo. You do not want management to ruin the product with aggressive monetization. You do not want them to turn the owl into a CAC machine.

But as an investor, I also have to be honest: this is less controllable than retention optimization.

Luis said it himself. Word of mouth is beautiful because it is free, but they do not have the same measurement and control they have with retention.

That is the risk.

L2C take aways and performance

I am still bullish on Duolingo long term.

The product is improving. AI is a real tailwind. The company is highly profitable. The balance sheet is strong. The learning ontology thesis is intact.

But Q1 made the main risk clearer.

The question is no longer: “Can Duolingo use AI to make the product better?”

I think the answer is yes.

The question is: “Can a better product restart top-of-funnel growth?”

That is much harder.

If the answer is yes, then $DUOL remains one of the most interesting consumer AI companies in the market. It would mean the company can use AI to improve teaching quality, increase engagement, expand monetization, and eventually reaccelerate user growth.

If the answer is no, then Duolingo may still be a very good business, but the multiple has to come down because the market will stop underwriting hypergrowth.

For now, I see Q1 as a yellow flag, not a red flag.

The business is not deteriorating. It is evolving.

Duolingo is becoming a much better teacher.

Now it needs to prove it can still find new students.

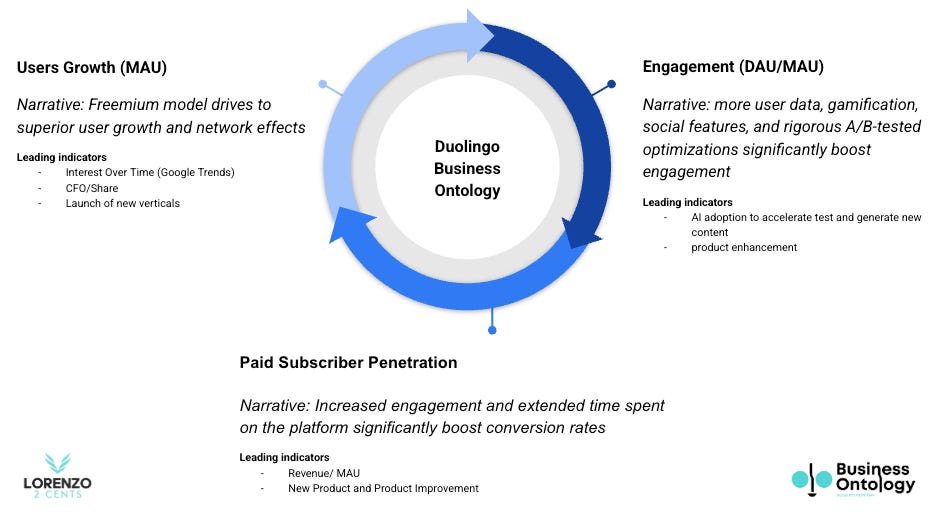

Looking at my Business Ontology visual, while Duolingo is performing well on the first two pillars (“Engagement” and “Paid Subscription Penetration”), it needs to improve a lot on User Growth.

As always, here is the “Deep Dive To Date” (DDTD), that is how the DUOL stock is performing since my initial deep dive on the January 11th 2025, when the price was $318.15.

-67% DDTDI remain long DUOL 0.00%↑ .

If you want access to:

My portfolio

all my trades in real time

my price targets and how I calculate them

Business Ontology content

My price targets will be shared in the Telegram Group and explained on my Youtube channel.

Please note that:

I can be and will be (hopefully not often) WRONG. This is just my personal strategy—NOT FINANCIAL ADVICE. I don’t know your financial or life situation well enough to give any recommendations. Please do your own due diligence and research. Don’t be LAZY.

Be the architect of your own destiny.

Ciao

Lorenzo

I like this. I need to be in your discord. Where can I access?

Very good analysis