HIMS: I am calling the bottom

$HIMS Q4 2025 ER Update

The content of this analysis is for entertainment and informational purposes only and should not be considered financial or investment advice.

HIMS business is going through two temporary headwinds, and both get better as 2026 progresses:

The book cleaning: the company cleaning up lower-quality / on-demand behavior

GLP-1 uncertainty (regulatory/legal noise around compounding)

On the GLP-1 side, Andrew Dudum (co-founder & CEO) was explicit that compounded GLP-1s are not the company:

the amount of patients that actually are on the compounded GLP-1s is actually quite a small minority of the aggregate subscriber base.

And in the prepared remarks, the company framed GLP-1s as a case study of a bigger shift:

Healthcare must evolve towards that same consumer-oriented distribution model.

So my bet is simple:

As GLP-1 distribution normalizes (especially with big pharma partnerships) and the book cleaning slows, the underlying platform growth shows up again.

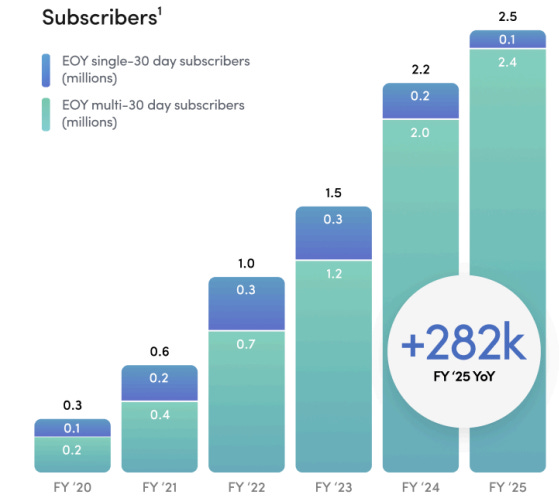

One more thing: your highest-quality users are the ones on a “monthly membership” behavior and when multi 30-day subscribers hit an all-time high (~96%), that’s a huge signal.

It means the base is increasingly made of loyal subscribers (not one-off buyers).

Table of Contents

Q4 2025 Update

L2C take aways and performance

Business Ontology Framework by L2C

Business Ontology

4D Valuation Model

L2C portfolio strategy

Q4 2025 Update

Scale + distribution: this is the real moat

This is the quote that matters most (from the earnings call).

It explains the “compounding” effect of scale:

To give you an idea of how our speed to market has changed, historically, we targeted launching one new specialty every year… Longer tenured offerings like sexual health and hair loss… took three and sometimes even four years to eclipse $100 million in annual revenue… our weight loss offering reached $100 million revenue run rate in less than seven months after launch…

Translation in plain English:

Once you have distribution, new specialties are not “new businesses”.

They are new entry points into the same machine.

It’s like Amazon.

First: books.

Then: everything.

Same logistics.

Same flywheel.

Labs is a Trojan horse

Labs matters because it creates:

a new entry point

higher engagement

better personalization

a reason to stay for years

Andrew Dudum (co-founder & CEO) described the direction very clearly:

as we’re able to get testing at home for cheaper, cheaper, cheaper cost… you as a member of Hims & Hers can be getting access to this type of data collection on a really frequent basis.

And Labs is already priced like a low-friction membership add-on, not like a luxury service.

In their Labs launch release, Hims offered:

Base plan: $199/year (50 biomarkers)

Advanced plan: $499/year (120+ biomarkers)

That’s absurdly cheap compared to what healthcare normally charges.

And it’s exactly why I call it a Trojan horse. It’s a no brainer.

If you acquire a customer with a $199/year bloodwork plan, you can later monetize with higher-value treatments where clinically appropriate.

Plus, in the prepared remarks, the company highlighted cross-sell potential:

we’ve identified that over 70% of lab customers may be eligible for treatment plans offered through the platform

Once you have the data, you have everything.

International: they’re telling you they will run near breakeven (on purpose)

Another important line from the call:

Across the majority of international markets, we expect to take a growth-oriented approach… even if that means running certain markets at or near breakeven on an adjusted EBITDA margin basis.

This is what good capital allocators say.

They are basically telling you:

“We will buy market share first, then optimize margins later.”

My take: the bottom is in

My thesis is simple:

GLP-1s demand is likely back

Book cleaning is easing

Hims is building the consumer health distribution layer

Labs increases engagement and personalization

GLP-1s are a catalyst, not the business

International is a long runway

The market tends to overreact to bad news, such as Novo Nordisk’s lawsuit.

But the platform keeps compounding.

This is why I’m calling the bottom, in terms of users and revenue growth.

Peptides: the business case

The key idea: peptides are likely to be another category expansion moment.

They fit perfectly with what Hims sells:

recurring relationships

ongoing clinical oversight

personalization

distribution at scale

Andrew Dudum (co-founder & CEO) literally put peptides in the roadmap:

…work on innovation and R&D for future categories like peptides which we’re working on right now.

On the regulatory side, Reuters reported the FDA was expected to lift restrictions on certain peptides used by compounding pharmacies (this is about compounding policy, not full FDA approvals for new drugs).

Example: BPC-157 (how it’s used, how recurring it could be, and a realistic serviceable market)

BPC-157 is probably the most famous “wellness peptide” right now.

What it is (in plain English):

OPSS (a U.S. Department of Defense program) describes BPC-157 as a lab-made synthetic peptide, often promoted to speed healing of wounds and injuries (skin, tendon, muscle, ligament, bone), and also marketed for gut/joint health and inflammation.

The FDA has listed BPC-157 among bulk substances that may present significant safety risks for compounding (Category 2 for 503A), citing limited safety information for proposed routes of administration and potential risks related to immunogenicity/impurities.

A systematic review (orthopaedic sports medicine) notes BPC-157 is not FDA-approved, but is still being used; the review found mostly animal evidence and very limited human evidence (one small retrospective human dataset was mentioned).

How it tends to be used today (the “workflow”):

Trigger: injury, pain, or “recovery optimization” (tendon/ligament issues, joint pain, post-surgery recovery, etc.)

Channel: cash-pay clinics / concierge medicine / compounding + wellness

Format: commonly discussed as injectable (subcutaneous / sometimes localized injections), and sometimes oral for “gut health” claims

Pattern: typically sold as a cycle (weeks), not as a forever drug

This is not a GLP-1-type subscription where someone stays on it for years.

It’s closer to:

a repeatable “course” product (like antibiotics, physio, or an MRI)

or a seasonal / episodic product (you come back when you’re injured again)

How recurring could it be:

There are probably 3 recurring paths Hims could realistically build around a peptide like BPC-157:

A) Injury recurrence = repeat cycles

If someone gets 1–2 injuries per year (or has chronic tendon issues), they may do 1–2 cycles per year.

That’s recurring, but episodic.

B) Subscription wrapper (the Hims way)

Even if the peptide is episodic, Hims could monetize a recurring relationship via:

ongoing “injury prevention + recovery” membership

access to providers

labs, biomarker tracking, or imaging referrals

adjunct products (sleep, pain, inflammation, PT guidance, supplements)

C) Bundled category expansion

BPC-157 is not the endgame.

The endgame is: “Hims becomes the consumer distribution layer for performance + recovery + longevity.”

BPC-157 is just one SKU in that shelf.

Potential market for Hims right now (based on their subscriber base)

Instead of guessing a top-down TAM, here’s the clean way to think about BPC-157 as a product inside the current Hims subscriber base.

Known input:

Subscribers at end of 2025: 2.5M+

Define the variables:

N = subscribers (use 2.5M)

a = adoption rate (share of subscribers who do at least one BPC-157 cycle)

f = cycles per year per adopting subscriber

if “every x months”, then f = 12 / x

P = price per cycle (cash-pay; depends on dosing + provider visit + fulfillment)

Then the annual revenue opportunity (gross) is:

Annual Revenue = N × a × f × P

Now plug in scenarios (these are assumptions, not facts):

Scenario A (conservative)

a = 1% of subscribers

x = 12 months → f = 1

P = $250 per cycle

Revenue = 2,500,000 × 0.01 × 1 × $250 = $6.25M/year

Scenario B (base case)

a = 3% of subscribers

x = 6 months → f = 2

P = $300 per cycle

Revenue = 2,500,000 × 0.03 × 2 × $300 = $45M/year

Scenario C (aggressive)

a = 5% of subscribers

x = 4 months → f = 3

P = $400 per cycle

Revenue = 2,500,000 × 0.05 × 3 × $400 = $150M/year

Even at modest penetration, this can become a meaningful incremental line item, but it’s not a GLP-1-sized engine.

And the real strategic value is still the same:

If a peptide brings people into the platform, Hims monetizes the relationship over time (labs, follow-ups, other categories), not only the peptide itself.

Why this matters for Hims:

If Hims can make any peptide category:

safer

more compliant

more standardized

and more subscription-wrapped

…they can turn a messy, episodic, cash-pay trend into a real platform business.

And importantly: BPC-157 is only one example.

Over the next few years, there are likely to be tens of peptides that get allowed / re-allowed in some form.

So the real opportunity is not “BPC-157 revenue”.

It’s Hims building the distribution + care layer that can keep adding new peptide SKUs as the menu expands.

L2C take aways and performance

The Hims thesis is more alive than ever, and the headwinds are slowly dissipating. Starting next quarter, I expect user growth to resume, with revenue following soon after.

As always, here is the “Deep Dive To Date” (DDTD), that is how the stock is performing since my initial deep dive on the February 8th 2025, when the stock price was $42.54.

-55% DDTDFrom here on, the content is restricted to L2C Premium Members, folks who’ve chosen to unlock this toolkit and support my independent research:

Business Ontology Framework by L2C

Business Ontology: My core blueprint for modeling and tracking company performance at every level.

4D Valuation Model: the valuation tool I use to value all my investments (Fair price is useless)

L2C Portfolio Strategy: My portfolio allocation and strategy in details

L2C Portfolio access & trades alerts: Real-time views into my holdings, plus instant notifications on buys, sells, and shifts.

Business Ontology Framework by L2C

The Business Ontology is a framework I built after tearing apart several tech companies from the ground up—breaking them down to their basic parts and piecing together a real thesis on what drives them. Think of it as a map of a company’s soul. It’s a tight set of core indicators—tailored to each business—that show if it’s heading the right way, no matter what the stock price says. These aren’t your basic stats like P/E ratios or revenue bumps you grab from Yahoo Finance. They’re deeper, sharper, and linked straight to the thesis I’ve cooked up on how the company makes value and fights in its market.

The framework boils down to two big pieces:

The Business Ontology—This checks if the company’s worth buying into or hanging onto.

The 4D Valuation Model—This gives you a 4D roadmap to guide your own calls on how much to put in (allocation).

Now, let’s dive into Hims and this quarter’s update.