Hims Is an AI Company - Few Got It

$HIMS Q1 2026 ER Update

The title of my last Hims update was simple: I’m calling the bottom.

I think that call was right.

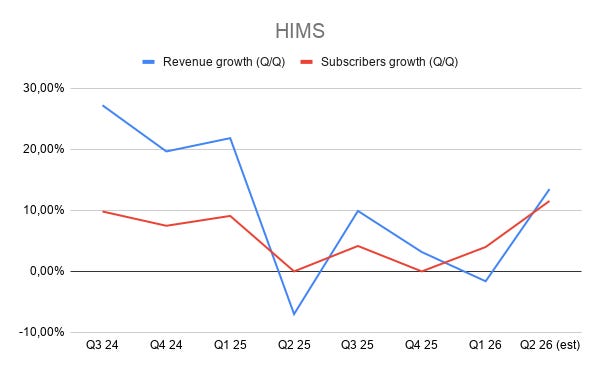

Q1 revenue grew only 4% year over year, gross margin compressed, and GAAP net income flipped to a loss. The quarter that Hims just reported is backward-looking.

The more important information came from the guidance, the Novo Nordisk pivot, the Eucalyptus deal, and especially what management said about AI.

And I think very few people have understood where Hims is going.

Management guided Q2 revenue to $680–700 million and raised full-year 2026 revenue guidance to $2.8–3.0 billion.

Yemi Okupe, Hims’ CFO, basically told investors that demand in weight loss is exploding again:

Within weeks of this launch, we are on track to add north of 100,000 new subscribers per month within our weight loss specialty. Early signs point toward a high level of subscriber engagement with nearly 90% of these users downloading the app and the average subscriber of these products interacting with the provider 3 times in the first month.

In Q4 2025, subscriber growth was almost irrelevant. In Q1 2026, Hims added roughly 100k subscribers in the quarter, or around 33k per month average.

Now management is talking about north of 100k new weight-loss subscribers per month.

That is roughly 3x the Q1 pace.

And this is happening after the strategic shift toward a broader assortment of FDA-approved GLP-1s through Novo Nordisk.

Hims announced in March that Novo Nordisk’s FDA-approved GLP-1 medications were available through the platform, including Wegovy options and Ozempic for eligible patients where clinically appropriate.

This matters because the market narrative on Hims became too simplistic.

The bear case was: “The compounded GLP-1 opportunity was temporary, so the business is broken.”

My view is different.

The compounded GLP-1 opportunity was the ignition. The real asset is the consumer healthcare distribution layer.

Hims can take demand, route it through a regulated medical workflow, connect it to providers, manage the customer relationship, and increasingly personalize the journey.

That is not easy to replicate.

Andrew Dudum also said demand is now stronger than what they saw during major seasonal campaigns:

We see it in the scale of new customers coming in the door today, which is larger than, as Yemi said, any spikes we saw even during the most important seasonal campaigns such as New Year’s and Super Bowl campaigns.

That is why I do not think Q1 is the quarter to obsess over.

The important signal is what happens from Q2 onward.

Hims is sandbagging

Management guided Q2 revenue to $680–700 million.

At the midpoint, that is around 13.5% sequential growth from Q1.

At the high end, it is around 15% sequential growth.

That already tells you the business is reaccelerating.

Now add the second part of Yemi’s comment:

...with record-level users coming to the platform, the focus really is on continuing to expand share, expand our reach and expand the overall subscriber base. And so with that, I think we would expect to see accelerating growth via revenue over the back half of the year.

For a subscription business, I read “accelerating growth” primarily as sequential acceleration.

If Hims does $700 million in Q2 and hits the high end of full-year guidance at $3.0 billion, then Q3 and Q4 together need to contribute about $1.692 billion.

One simple version could be:

Q1: $608 million actual

Q2: $700 million high-end guidance

Q3: $800 million

Q4: $892 million

FY 2026: $3.0 billion

The problem is that this would not really show clean acceleration into Q4. It would imply Q3 growing about 14% sequentially and Q4 growing about 11% sequentially.

So if management is serious that the back half should accelerate, and if monthly subscriber additions really are running north of 100k in weight loss alone, then the full-year guide looks conservative to me.

This is not a precise model. I am not pretending to know Q3 and Q4.

But the direction is clear.

Hims is guiding to a year where growth reaccelerates, while also telling us that the biggest category is seeing record-level demand. That combination does not sound like a business in structural decline.

It sounds like a business sandbagging a little.

And this excludes Eucalyptus.

Hims valuation in 2027

The Eucalyptus acquisition is also important.

Hims announced the deal in February. Eucalyptus is a consumer healthcare platform with operations in Australia, the UK, Germany, Japan, and Canada. Hims disclosed that Eucalyptus had an annual revenue run-rate north of $450 million and delivered triple-digit year-over-year ARR growth in every quarter of 2025, while operating within line of sight of profitability.

The transaction is expected to close around the middle of 2026, subject to approvals, and Hims explicitly excluded any Eucalyptus contribution from its Q2 and full-year 2026 guidance.

This means the reported guidance does not fully capture the new international scale.

If Hims exits 2026 near a $3 billion revenue run-rate and then layers in Eucalyptus, which was already north of $450 million ARR and growing very fast, the combined business could be much larger than what the current headline guidance implies, probably around $4 billion revenue run-rate in 2027.

At around a $6 billion market cap, it sounds a great deal to me.

No financial advice, of course. Do your own work.

Hims is an AI company and providers are training the model

Now we get to the part that I think almost everyone is missing.

Hims is an AI company.

I know this sounds like a cliché because every company now says it is an AI company.

But with Hims, the claim is not marketing.

It is structural.

In my first Hims deep dive in February 2025, I framed one of the key points as: a critical factor in leveraging the quantum leap in AI technology.

The idea was simple.

Healthcare AI is only as good as the feedback loop behind it.

You need consumer intent. You need symptoms. You need diagnosis. You need provider decisions. You need treatment plans. You need side effects. You need outcomes. You need longitudinal data. And you need all of that in one system.

Most healthcare companies do not have this.

Hims does.

Mohamed ElShenawy, Hims’ CTO, explained it clearly on the call:

We’ve embedded intelligence at every step of the care journey, while keeping independent providers responsible for all clinical decision-making. For example, we currently have an AI copilot live on the provider side of the platform that drafts contextual responses on behalf of our care coaches, which are then reviewed by the care coaches before being sent.

This is exactly the loop.

AI drafts. Humans review. Humans correct. The system learns.

And then he made it even more explicit:

We currently support tens of millions of customer touch points annually and independent providers view, correct and approve AI inputs that make up our platform design. This means we are generating clinician-verified training signals for our models. This is the highest quality label in AI any company can hope for, and it can’t be acquired.

That sentence is the whole thesis.

Clinician-verified training signals.

This is not generic web data. This is not scraped text. This is not a chatbot guessing from public medical information.

This is real healthcare workflow data, corrected by providers, attached to actual patients and outcomes.

That is very hard to buy.

It has to be earned through volume, trust, workflows, regulation, and time.

And Hims has been building it for years.

I want to be much more direct here.

Providers are training the Hims AI model.

Yes, today providers remain responsible for clinical decisions. They have to. Healthcare is regulated, sensitive, and high trust.

But look at the architecture.

Hims is not simply adding ChatGPT on top of a telehealth workflow. Hims is building the workflow so the human provider corrects, approves, rejects, escalates, and labels what the AI does. That is exactly the feedback loop you need if your goal is to train proprietary healthcare models.

Here is the important part: providers are training the system that could automate a large part of provider work over time: AI handles the repeatable part, guardrails decide what can be done automatically, escalation rules decide what needs a clinician, and the clinician keeps improving the system every time he or she intervenes.

This is why I think Hims will eventually train at least two kinds of proprietary models.

First, a model to predict disease risk or likely conditions from symptoms, clinical history, labs, wearables, medication response, side effects, and outcomes. This may not even be a classic LLM. It could be a more specialized model, maybe an encoder-style system, because the task is not “write me a nice paragraph.” The task is: given this patient profile, what is probably going on?

Second, a model to recommend the next best treatment path from symptoms, history, predicted disease, prior responses, contraindications, and outcomes. In other words: if this is the likely problem, what should the platform suggest, prescribe, monitor, or escalate?

There can still be a frontier model as the orchestrator. There can still be a 24/7 companion talking to the subscriber. But the real IP, in my opinion, is not the chat interface. The real IP is the clinical prediction and treatment-decision layer trained on Hims’ own loop.

Management is already pointing in this direction.

Labs AI explains biomarker results in the unique context of each customer, flags what matters, and knows when to recommend escalation to a provider.

The AI weight-loss companion will proactively support customers, reach out at the right moment, and prompt clinician engagement when needed.

Providers are in the loop more to review and validate what AI does or would do, rather then the other way around. That is the architecture of an AI-native healthcare company.

Hims is not selling prescriptions online.

Hims is building an intelligent care layer between the consumer, provider, medication, lab result, wearable, side effect, and outcome.

That is a completely different business.

Switching cost as a function of time

I have a personal example I want to share.

I built a system based on Hermes Agent, which I call Max, to track what affects my health.

Max lives on a Mac mini. He has access to my Obsidian notes and my Google Sheets database. I speak to him on Telegram. He knows my diet, my habits, my baseline routine, and every day he asks me if I have anything to declare that deviates from normal.

It can be food, training, symptoms, sleep, supplements, anything worth registering.

I send a voice note and he logs it.

Every six months, I do blood work. I send Max a picture of the results and he helps me record the markers in the database.

The goal is simple: correlate what I do with how my biomarkers change, and then improve the markers over time.

For example, from October 2025 to May 2026, my testosterone increased from 3.89 to 5.1, probably helped by keto/carnivore, more sun, and heavy lifting.

This is useful.

But 99.9% of people will never build something like this.

They do not want to manage notes, spreadsheets, automations, reminders, and lab data.

They want the outcome.

If Hims can make this kind of proactive health companion easy, cheap, regulated, and personalized, then the value proposition becomes much stronger than “buy this treatment online.”

It becomes: stay on the platform because the platform knows you better every month.

The longer you stay, the more data you accumulate.

The more data you accumulate, the more useful the recommendations become.

The more useful the recommendations become, the harder it is to leave.

This is switching cost as a function of time.

And it is also a network effect, because every patient interaction, provider correction, treatment journey, and outcome can improve the system.

That is why Hims could become much more defensible than people think.

Hims building a moat

Management basically described the same flywheel:

With this infrastructure, we are strengthening the closed-loop proprietary data flywheel that competitors cannot recreate. We are one of the only platforms in healthcare where consumer intake and diagnosis, treatment journey, provider decisions and eventual outcomes all live in a single stack, and we’ve designed our platform to get stronger as these insights grow.

This is exactly what I want to own.

Not just a digital clinic.

A full-stack healthcare data loop.

Intent → intake → diagnosis → treatment → titration → side effects → outcomes → better models → better care → more customers → more data.

That is the flywheel.

And because Hims is consumer-first, the company is not waiting for employers, insurers, hospitals, or legacy systems to move.

It goes directly to the person who wants to feel better.

This matters.

The traditional healthcare system is not designed around consumer delight. It is slow, fragmented, and reactive.

Hims is trying to make healthcare feel more like a high-frequency consumer product.

That is why I think the company can win share in markets like weight loss, sexual health, dermatology, mental health, longevity, labs, and eventually broader preventive care.

The more categories they add, the more complete the customer profile becomes.

The more complete the profile becomes, the more valuable the intelligent layer becomes.

This is why the Eucalyptus acquisition also matters strategically, not just financially.

Different geographies mean different populations, disease profiles, regulations, medications, and care patterns.

That can make the model better.

Hims said it directly:

We believe our global scale will act as a force multiplier with models reflecting the populations, disease profiles and care patterns of multiple geographies, fundamentally improving the intelligence we are building.

This is the part I think investors are underestimating.

The data advantage is not just US GLP-1 demand.

It is global, multi-category, longitudinal consumer health data inside a regulated care workflow.

Lorenzo2cents (L2C) take aways and performance

I have never been more excited about Hims.

The vision and the catalysts are finally coming together at the same time.

GLP-1 demand is reaccelerating. Novo gives Hims a cleaner regulatory path. Eucalyptus adds international scale. Guidance looks too low. The AI/data flywheel is no longer hidden in the background. Labs, wearables, biomarkers, companions, and provider-verified training signals are turning Hims into something much bigger than a telehealth app.

This is the strongest version of the Hims thesis I have seen so far.

My position is fully built at around 10.3% of my portfolio.

But if the market gives me another dislocation, I could still use options to take advantage of it.

I do not own Hims because of a temporary GLP-1 trade.

I own Hims because I think it can become the default consumer healthcare platform for people who want to feel good, perform, lose weight, optimize biomarkers, and live longer.

That is a massive market.

And if Hims is right on the AI layer, this can become a winner-takes-most business.

As always, here is the “Deep Dive To Date” (DDTD), that is how the stock is performing since my initial deep dive on the February 8th 2025, when the stock price was $42.54.

-39% DDTDIf you want access to:

My portfolio

all my trades in real time

my price targets and how I calculate them

Business Ontology content

My price targets will be shared in the Telegram Group and explained on my Youtube channel.

I share my thoughts on X.

Please note that:

I can be and will be (hopefully not often) WRONG. This is just my personal strategy—NOT FINANCIAL ADVICE. I don’t know your financial or life situation well enough to give any recommendations. Please do your own due diligence and research. Don’t be LAZY.

Be the architect of your own destiny.

Ciao

Lorenzo