Lemonade: all key metrics are trending positively

$LMND Q3 2024 ER Update

All key metrics are trending positively, which the market recognized, likely leading to a squeeze on short traders.

As of October 15, LMND 0.00%↑ had a short interest of 32.58% on its float. Following the earnings release on October 31, the stock closed up by 26.77%.

If you haven't read my original deep dive on Lemonade, I recommend doing so before reviewing this update. It's essential reading for a thorough understanding of the company.

Let’s break down some of the most relevant results from this quarter.

Lemonade’s growth story remains strong: the In-Force Premium (IFP) grew 24% year-over-year to $889 million in Q3, accelerating from 23.64% growth in the previous quarter. Additionally, Lemonade has raised its full-year guidance for gross earned premium and revenue, while reaffirming its FY 2024 guidance for all other metrics.

Management's strategy to reduce CAT impact is delivering results: the gross loss ratio for the quarter was 73%—the strongest outcome in four years—helping to further drive down the trailing twelve-month (TTM) gross loss ratio.

Daniel Schreiber, co-founder and CEO of Lemonade on the matter:

For the fourth consecutive quarter, we saw double-digit improvements in the loss ratio compared to the same quarter 1 year prior, and our loss ratio is now back where we like to see it, comfortably within our target range. How have we done it? …diversification of the portfolio and intense and sustained efforts in matching rate to risk across the portfolio and across the U.S. All this enabled us to deliver notably expanded gross margins in Q3.

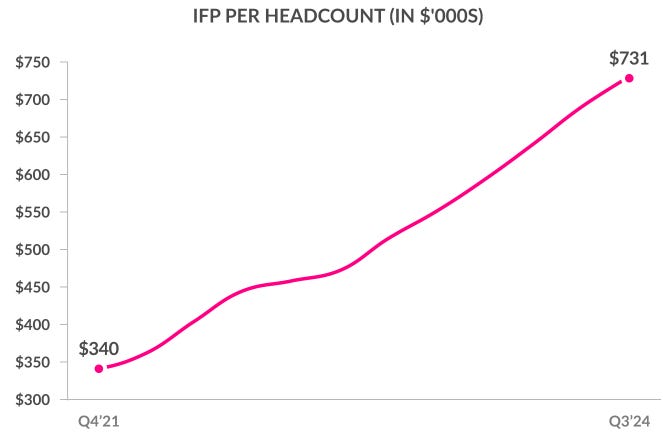

Lemonade's AI operating system continues to drive efficiency: Interestingly, Lemonade has included in its shareholder letter the same metric I calculated in my original deep dive: IFP per headcount. This metric shows that the company is becoming increasingly efficient over time.

Furthermore, Lemonade maintained a solid score of 43 under my custom Rule of 40 metric, confirming that the AI engine is effectively optimizing both growth and profitability.

Specifically looking at the loss ratio, this quarter there was a wider-than-usual gap between the gross and net ratios—73% versus 81%—which I expect will be narrowed in the next quarters. This improvement should further enhance the net loss ratio and, consequently, the Rule of 40 score.

Timothy Bixby, Chief Financial Officer of Lemonade, answer a question on this specific topic:

It was a little wider than usual. And then on occasion, it's been narrower than usual. I think we've had a few quarters that would have been identical or within a point or normal is somewhere in between…

…I'd expect the difference to be in the low single digits more consistently, 3 or maybe 4 points typically, but it does vary from that.

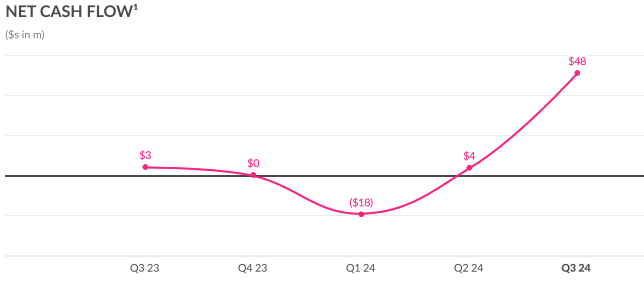

Cash Flow: The company once again delivered a Net Cash Flow (NCF) positive quarter, generating $48 million. Cash Flow from operations was positive in the third quarter at $16 million. The management reiterates its expectation of achieving sustainable NCF positivity by the end of the year.

Annual dollar retention continues to improve year over year, affirming that Lemonade's competitive moat remains strong.

Timothy Bixby explained why this metric is slightly down compared to the previous quarter.

Annual dollar retention was 87% up 2 percentage points since this time last year and down slightly versus 88% in the prior quarter. This slight sequential decline is as expected, given our efforts to reduce less profitable portions of our home book in the second half of this year.

Like many of you, one question I often consider when evaluating Lemonade's competitive moat is whether legacy insurers could eventually catch up to Lemonade’s AI capabilities. Shai Wininger, co-founder and President of Lemonade, addressed this point during the Q&A as follows:

Legacy insurers have been outsourcing data science and AI work for over a decade. Yet despite these costly efforts, consumers haven't really noticed major changes in experience or insurance pricing. I believe there are many reasons for this lack of progress, such as the challenge of changing century-old processes and culture in organizations that are highly conservative by design. Anyone who worked for a large corporation knows how resistant to change and risk averse these organizations can become. Implementing AI and automation is even harder because these are advancements that threaten job security and demand new skills from seasoned employees.

Insurers weren't founded as tech companies, and so they rely on traditional vendors to provide essential systems. And since no single system runs an entire insurance company end-to-end, they're forced to work with dozens, if not more, of third-party providers. Creating a seamless AI-powered experience that delivers personalized customer interactions, improves efficiency and drives better underwriting and pricing require a unified full stack system with AI at its core.

Unlike traditional insurers, the Lemonade platform was designed, built and maintained in-house, and I believe this is our secret weapon. Blender, our insurance operating system, integrates everything, from customer interactions on our app, websites or phone to advertising attribution, customer segmentation, LTV modeling, pricing, underwriting, claims and more. I believe this level of control coupled with a team passionate about progress and change gives us an unfair advantage and a defensible moat that's hard to replicate.

My conviction in this company remains strong. Despite a 40% increase in stock price since my deep dive was published on September 24, I believe it is still valued as if facing a worst-case scenario—indicating there’s still room for further price growth!

See you in the next update ;)