Lemonade’s Q4 Surge: Hits Record-Low Loss Ratio, Revs Up for a Car Insurance Boom

$LMND Q4 2024 ER Update

The content of this analysis is for entertainment and informational purposes only and should not be considered financial or investment advice. Please conduct your own thorough research and due diligence before making any investment decisions and consult with a professional if needed.

The fourth quarter represents the fifth consecutive quarter of accelerating revenue growth for Lemonade, achieving an In Force Premium (IFP) of $944 million. This reflects a 26% year-over-year increase, aligning with the company's trajectory toward what its management has termed "cruising velocity"—a sustained annual growth rate in the 30% range, anticipated to begin in 2026 and continue in the years ahead.

Exceeding its own prior guidance and expectations, the company achieved an adjusted free cash flow of $27 million in Q4, marking its strongest performance to date. This result contributed to an overall cash flow positive year in 2024, with a total of $48 million, making it the company's first cash flow positive year.

If you haven't read my original deep dive on Lemonade, I recommend doing so before reviewing this update. It's essential reading for a thorough understanding of the company.

To address investors’ rising expectations for the car insurance business, indicated during the November 2024 Investor Day as the next engine of growth, Lemonade’s management dedicated part of the earnings call to responding to related questions, with their key points summarized as follows.

The company is taking a cautious approach to scaling its car insurance business, as articulated by the President and Co-Founder Shai Wininger and the CEO and Co-Founder Daniel Schreiber, while affirming that everything remains on track with the plan shared at the Investor Day.

Wininger emphasized stabilizing the loss ratio, stating:

We're in the process now of shifting from car as a declining business in terms of customer count, but a very stable business in terms of in-force premium to a point now where our loss ratios have come down significantly over the past year. It's not quite at our target, but it's getting awfully close.

Schreiber reinforced this restraint, highlighting the need for a solid foundation amid strong demand:

We've seen a tremendous amount of pent-up demand for our car product. We kind of spoke in broad terms about how we're still holding it back a little bit. […] But before we unleash rapid growth, we have to make sure that everything is solid. We've seen car growth run away from companies that haven't got all the foundations in place. We're keen to not let that happen to us.

He added that testing throughout 2025 will pave the way for significant growth—potentially in the billions—once stability is assured, with optimism for hitting key thresholds by year-end.

This progress supports their long-term vision of car insurance reaching 40% of the portfolio.

This dual focus on loss ratio control and rigorous testing reflects a strategy to avoid pitfalls while aligning with the Investor Day roadmap, ensuring a robust launch when conditions are optimal.

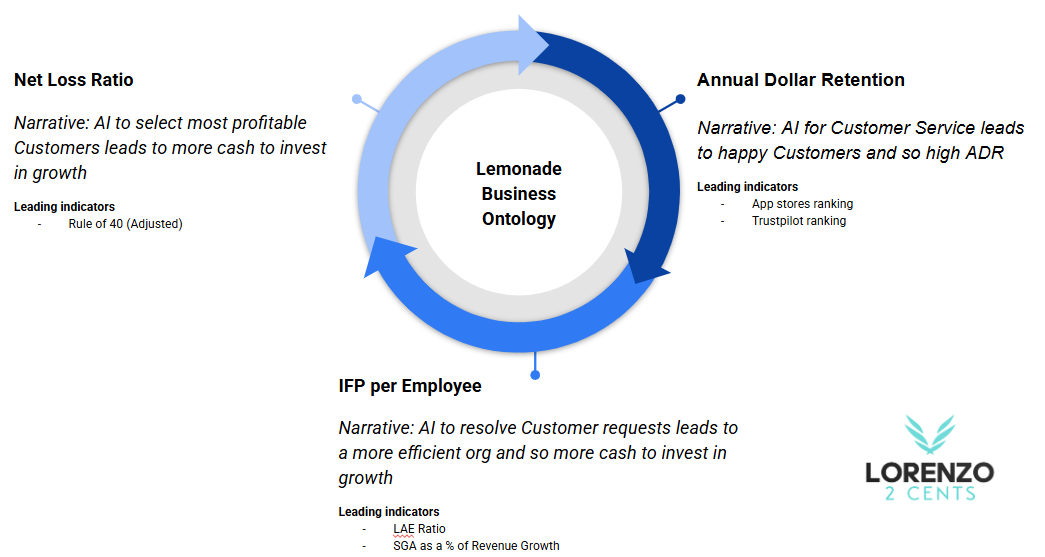

Lemonade Business Ontology

As with all the stocks I cover, I’ve developed a blueprint to monitor Lemonade’s business performance, aligned with my recently introduced Business Ontology Framework.

The core of my thesis on Lemonade hinges on two fundamental questions:

Can AI transform the insurance industry?

And, is Lemonade the AI-driven insurance company driving this transformation?

Of course, the answer must be “yes” to both.

My investment in Lemonade stems from my belief that its AI-powered operating system provides a competitive advantage that rivals will struggle to replicate for years to come. Consequently, the Business Ontology will primarily concentrate on evaluating the effectiveness of this AI system, as I anticipate it will ultimately drive exponential growth in cash flow per share and, in turn, deliver substantial stock price returns.

Below is a visual representation of Lemonade’s Business Ontology, presented in a clear and structured format.

Next, I dedicate a paragraph to providing an update on each component of the Ontology.

Annual Dollar Retention

During the earnings call, the CFO Timothy Bixby stated,

Annual dollar retention or ADR was 86%, down one percentage point since this time last year. This slight sequential decline in year-on-year decline is not unexpected, given our efforts to reduce less profitable portions of our home book in the second half of 2024. These efforts likely dampened our ADR by about three percentage points.

From this explanation, it can be inferred that, when adjusted for the impact of refining the home book, Lemonade’s ADR would rise to 89%, the highest ever achieved by the company. This figure stands out as exceptional when compared to the insurance industry’s average customer retention rate of 84%, as detailed in my original Lemonade deep dive.

Lemonade’s customer reviews on Trustpilot and app stores—metrics I view as key predictors of retention—further underscore the company’s success in satisfying its customers:

App Store (iPhone) rating: 4.9/5

Play Store rating: 4.5/5

Trustpilot rating: 4.2/5

IFP per Employee

Lemonade’s operational efficiency showed notable progress in Q4, with In Force Premium (IFP) per employee steadily rising toward an impressive $1 million per employee—a figure that underscores the company’s scalability.

The annual report highlighted a stark contrast in efficiency metrics as of December 31, 2024. Based on public data from five competing U.S. insurance companies, their estimated customers per employee ranged from approximately 150 to 450, adjusted for comparability and including agents and brokers as a significant cost factor. Meanwhile, Lemonade reported approximately 2,000 customers per employee, reinforcing its AI-driven edge.

Still on the operations efficiency, Loss adjustment expenses (LAE), excluding prior quarter adjustments—costs tied to investigating, managing, and settling claims—continued their downward trend, dropping to 8% from 9% over the past four quarters. This decline signals the increasing effectiveness of Lemonade’s CX.AI bot, which resolves customer inquiries instantly without human involvement.

Finally, over the long term, a key focus remains on reducing Selling, General, and Administrative (SGA) expenses as a percentage of revenue growth—a reliable sign of an effective growth strategy. A declining SGA ratio would indicate Lemonade is lowering the cost of revenue expansion, positioning it to outpace established competitors (see my comparison analysis in my original deep dive).

However, 2024 saw this positive trend stall, likely due to several factors:

Home Book Adjustments: Efforts to shed less profitable, high-catastrophe-risk customers impacted Annual Dollar Retention (ADR). Higher retention (ideally near 100%) would convert sales and marketing efforts directly into customer and revenue growth, whereas lower retention requires replacing churned revenue.

Customer Acquisition Focus: Lemonade in 2024 prioritized growing its customer base over cross-selling, as evident from the graph above.

Economic Factors: With inflation lower in 2024 than in 2022 and 2023—years when this KPI hit its lowest—premium price growth and investment income likely softened, and so the revenue growth.

CEO Daniel Schreiber provided clarity on growth spend during the earnings call:

I would expect it to continue to grow in absolute terms, but not to grow in percentage terms at the magnitude you've seen last year, '23 into '24 and '24 into '25. So in absolute terms, we will grow, but the growth rate will decline. And that's really what enables us to kind of keep all of the parts in balance as we get to that EBITDA breakeven point. When we see LTV to CAC improving or we see some positive impact, then we're able to kind of increase that growth spend proactively, and we're able to do that. We've done that in the past. But right now, that is our assumption based on what we know today.

In essence, Lemonade aims to optimize Lifetime Value to Cost of Customer Acquisition (LTV:CAC) before ramping up growth investments.

And when asked about prioritizing cross-selling for efficiency, Schreiber added:

Short answer is yes. I think that's absolutely true. And over time, that ability to cross-sell and upsell customers and the efficiency of doing that will increase as you go from -- we've gone from 1 million customers to 2 million, now we're heading to 3 million. That will only increase over time. Whether we would choose to keep it dead flat at zero, that's a choice we can make. But absolutely, that theme and that trend, you're right on.

This confirms a strategic shift toward cross-selling as the customer base grows, enhancing long-term efficiency.

Lemonade’s Q4 performance highlights its AI-driven operational strengths, though challenges like SGA trends warrant close monitoring as the company balances growth and profitability.

Net Loss Ratio

In my initial deep dive, I described the “AI-powered loss-ratio optimization” as the missing cherry on top, noting that clear evidence of its success had yet to emerge. That’s no longer the case. In Q4, Lemonade’s gross and net loss ratios plummeted to 63% and 62%, respectively—outstanding figures in absolute terms and even more striking given the downward trend.

Trailing twelve months (“TTM”) gross loss ratio came in at 73%, in line with Lemonade target range, 12 points improved vs prior year and 4 points improved sequentially. This marks the sixth consecutive quarter of sequential improvement in the TTM gross loss ratio.

To gauge the effectiveness and efficiency of Lemonade’s AI-driven strategy, I’ve updated my adapted Rule of 40, a metric that balances loss ratio and growth. In this version, I combine In Force Premium (IFP) growth with ‘1 minus the Net Loss Ratio’ to assess the trade-off.

In Q4 2024, Lemonade achieved a score of 64, reflecting significant quarter-over-quarter and year-over-year gains in both In Force Premium (IFP) growth and loss ratio. This impressive leap underscores the strengthening impact of its AI advantage.

Conclusion

Analysis through my proprietary Business Ontology Framework reaffirms that my thesis on LMND 0.00%↑ remains solid. I now look for In Force Premium (IFP) growth to approach the management’s target of 30% year-over-year, alongside a strong takeoff of the car insurance business in 2025, which promises to drive sustained growth in the years ahead.

As always, here is the “Deep Dive To Date” (DDTD), that is how the stock is performing since my initial deep dive on the September 24th 2024.

+100% DDTD

Stay tuned for the next update!

Thanks for the writeup! They have performed well last 6 quarters. It will be interesting to see how their GLR will develop next 4 quarters and will they improve their cross selling. Still less than 5% of their customers have multiple policies.