Lemonade: Innovator's Dilemma—Squared

$LMND Q4 2025 Earnings Update

The content of this analysis is for entertainment and informational purposes only and should not be considered financial or investment advice. Please conduct your own thorough research and due diligence before making any investment decisions and consult with a professional if needed.

I read the transcript rather than listening to the call, so I can’t be certain of Daniel Schreiber’s tone. But to me, this opening statement was clearly directed at the perma-bears who have insisted since day one that Lemonade will never be profitable:

Somewhat unusually, insurance is a business that tends to turn cash flow positive before GAAP accounting positive. The one almost inevitably follows the other. This then is as good a spot as I need to reiterate a long-standing expectation that we will be EBITDA profitable in Q4 of this year and EBITDA positive for the full year of 2027.

Table of Contents

Q4 2025 Update

Lorenzo2cents (L2C) take aways and performance

Business Ontology Framework by L2C

Business Ontology

4D Valuation Model

L2C portfolio strategy

Q4 2025 Update

By any measure, Q4 2025 was Lemonade’s strongest quarter ever. It was characterized by growth acceleration, underwriting excellence, and operating leverage—concluding a year in which momentum continued to build across key business drivers, as management explained.

At this point, I have no doubts that the data moat is real and working. This is visible not only in the numbers but also in Daniel’s words, as he described how the flywheel works—as if to say, “Yes, now we’re certain it really works.”

We continue to be highly focused on growth and accelerating growth because it’s a gift that keeps on giving. Faster growth drives better data and further sharpens our segmentation and pricing capabilities. This powers improving underwriting performance and rapid gross profit growth and we can swiftly redeploy gross profit, thus generated into profitable growth investments with compelling unit economics and so the cycle continues. It’s energizing to see the flywheel continue to compound even as we scale. What’s particularly encouraging is that all this progress is broad-based. Pet, car and [ Europe ] are all coming into their owner’s powerful growth drivers, each combining hyper growth with improving underwriting performance.

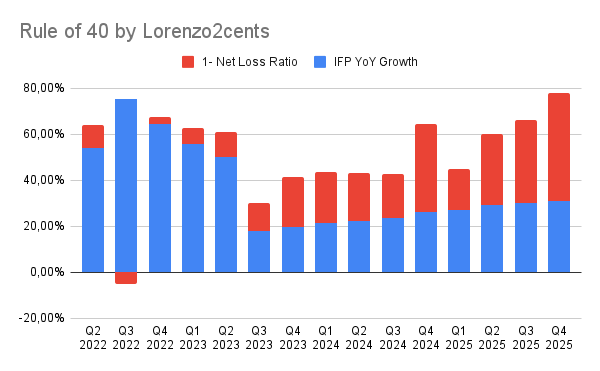

The best way to illustrate the perfection of these earnings is to share my updated custom Rule of 40, where I sum the IFP growth rate with “1-Net loss ratio”. The higher the better.

Gross profit and its growth lie at the heart of efforts to optimize IFP growth and the loss ratio. The trend shows that Lemonade has navigated this trade-off beautifully. But even more surprisingly, when you’d expect this metric to eventually flatten, Q4 printed an all-time high of 78—surpassing the value from Q3 2022, when the company was a hyper-growth startup with half the IFP.

This is truly surprising and exceeds even the best expectations. While 31% IFP growth was guided, you’d expect the loss ratio to stay flat or potentially worsen. The fact that Lemonade keeps improving both metrics simultaneously means my thesis is playing out perfectly: Lemonade is poised to disrupt a 300-year-old insurance industry.

Innovator’s Dilemma—Squared

Lemonade is leveraging one innovator’s dilemma, and soon they’ll leverage a second.

Regarding the first, here’s Shai speaking about incumbents in response to a question on how Lemonade can stay ahead of competition:

…companies built on the foundation of people, not technology. They treat tech as a cost center, not their core. They rely on third-party vendors that are themselves built on legacy systems which leaves insurers with hundreds of these connected systems, they need to run their business.

It’s very hard for an organization like that to compete with a full stack tech-first company like Lemonade. In fact, in the history of all tech resolutions, you can probably count on the fingers of one hand, there are companies that dominated prior to the tech revolution and still were there in a dominant position after that. It would be naive to expect the incumbents will be in this place forever. Of course, they are already talking about increasing investment in AI, ensuring a case study here and there. But by the time they make meaningful progress, we believe we’ll always be several steps ahead.

For those who’ve worked in big corporations, this is obvious. For everyone else, it will be obvious in hindsight.

It’s not just about the data flywheel that Lemonade built through its counter-positioned D2C approach. It’s also about the people. Lemonade’s employees embrace AI and enable efficiencies that incumbents can only dream of. Incumbents are dinosaurs and will likely go extinct or become irrelevant. This is life—it always happens, and this time is no exception. It starts from the top. You can’t expect a CEO of a 100-year-old insurer to radically change how they operate, even if he knows it’s the right thing to do. It would mean laying people off and radically changing internal politics built over decades that defend the status quo—with the risk of failure. This simply can’t happen at scale for incumbents.

Now, to the second disruption.

The economy is transforming quickly and will be radically different in a few years. People can’t realize it because they think in linear terms, but it’s very clear to the tech-savvy who work with technology daily that we’re reaching an inflection point. We’re only a few weeks into 2026 and already around 20–25 new LLMs or significant variants have launched—not to mention OpenClaw, which democratizes agentic capabilities, allowing anyone to easily build use cases to automate daily tasks.

While this technology will take years to radically change how large enterprises work, new AI-native startups will emerge quickly and eat the incumbents’ lunch.

This will result in a profoundly changed economy, where more and more “transactions” will be executed by AI agents, not humans.

The easiest way to visualize this is through autonomous cars, which are already here. Autonomous cars don’t just drive themselves—they’ll increasingly maintain themselves.

They go to recharge and pay for it themselves.

They drive on the highway and pay the tolls themselves.

Project this trend onto robots in general, and it becomes even clearer. Think about humanoid robots, which we’ll likely have at scale in 3 to 5 years. They’ll do tasks on our behalf, which means they’ll take risks. When doing laundry, they may damage our clothes. When walking on the street, they may hurt people or damage objects. Every autonomous object will carry potential liability that needs to be mitigated.

Now, how do you think this will work? Do you think a robot’s owner will visit an insurance agency to ask for a quote to cover the robot for certain activities?

When you stop laughing, you can keep reading!

Autonomous objects will get insurance autonomously, based on the activity they’re about to perform, in seconds.

Which company is poised to capture most of this trillion-dollar business?

You name it.

Lemonade has already proven its willingness to be first by taking the risk of insuring Tesla cars driven by FSD.

If the car becomes better and safer with software updates or hardware upgrades our pricing will automatically respond and continue to drop.

As of this moment, autonomously driven miles using Tesla’s [ FSD ], priced at about 50% of the equivalent human-driven miles. So we expect this to get better over time. We believe this represents a fundamental shift for the industry. As autonomous driving becomes safer and more widely adopted, prices should fall transparently and dynamically.

Shai Wininger said something else during the earnings call, and I believe he chose his words carefully.

As physical objects such as vehicles increasingly shift from being controlled by humans to being operated by AI, insurance needs to evolve as well.

Autonomous cars are just the beginning.

Lorenzo2cents (L2C) take aways and performance

My thesis on Lemonade—growth with near-zero marginal costs—is fully unfolding. As of now, there’s not a single reason to doubt that 30% IFP growth for the foreseeable future, as guided by management, is achievable.

Even more, Lemonade is positioning itself to conquer a totally new market: autonomous agents & objects, which will be even bigger than the current insurance industry. If Lemonade captures a 5% market share of the US Property & Casualty (P&C)/Auto Insurance/autonomous objects market in 10 years, it will likely be a $1 trillion company.

As always, here is the “Deep Dive To Date” (DDTD), that is how the stock is performing since my initial deep dive on the September 24th 2024, when the stock price was $17.23.

3.3x DDTDFrom here on, the content is restricted to L2C Premium Members, folks who’ve chosen to unlock this toolkit and support my independent research:

Business Ontology Framework by L2C

Business Ontology: My core blueprint for modeling and tracking company performance at every level.

4D Valuation Model: the valuation tool I use to value all my investments (Fair price is useless)

L2C Portfolio Strategy: My portfolio allocation and strategy in details

L2C Portfolio access & trades alerts: Real-time views into my holdings, plus instant notifications on buys, sells, and shifts.

Business Ontology Framework by L2C

The Business Ontology is a framework I built after tearing apart several tech companies from the ground up—breaking them down to their basic parts and piecing together a real thesis on what drives them. Think of it as a map of a company’s soul. It’s a tight set of core indicators—tailored to each business—that show if it’s heading the right way, no matter what the stock price says. These aren’t your basic stats like P/E ratios or revenue bumps you grab from Yahoo Finance. They’re deeper, sharper, and linked straight to the thesis I’ve cooked up on how the company makes value and fights in its market.

The framework boils down to two big pieces:

The Business Ontology—This checks if the company’s worth buying into or hanging onto.

The 4D Valuation Model—This gives you a 4D roadmap to guide your own calls on how much to put in (allocation).

Now, let’s dive into Lemonade and this quarter’s update.

Business Ontology

Here’s a quick visual on the Business Ontology for Lemonade.