Lemonade: Car Accelerates

$LMND Q1 2025 ER Update

LMND 0.00%↑ kicked off 2025 with a solid Q1, continuing its growth trajectory while advancing toward profitability. In-force premium (IFP) reached $1,008 million, up 27% year-over-year, marking the sixth consecutive quarter of IFP growth acceleration (see chart below). This acceleration, from 18% in Q3 2023 to 27% in Q1 2025, reflects Lemonade’s ability to scale its customer base and deepen product penetration. Customer count grew 21% to 2.54 million, and premium per customer rose 4% to $396, driven by a mix of rate increases and cross-selling momentum. Revenue climbed 27% to $151.2 million. With $1 billion in cash and investments, Lemonade remains well-capitalized to fuel its ambitious roadmap, particularly in new product lines like car insurance.

If you haven't read my original deep dive on Lemonade, I recommend doing so before reviewing this update. It's essential reading for a thorough understanding of the company.

Lemonade Car

As Lemonade Car is poised to be the growth engine of the next decade for the company, and with Q1 2025 marking another step forward, it’s time to dedicate a recurring paragraph to track its progress.

The Car segment is gaining traction, with Chief Product Officer Michal Langer stating,

Lemonade Car continued to build momentum this quarter, and for the first time, its quarter-over-quarter IFP growth outpaced the rest of the business. That’s a key milestone and one that signals the engine is starting to rev,

Key drivers include Lemonade’s proprietary AI and telematics, which target young, safe drivers with precision pricing, and a massive cross-sell opportunity, with “nearly 2.5 million non-Car customers who together spend north of $3 billion annually on auto insurance.”

The day-zero telematics initiative is a game-changer here, aiming to integrate driving data insights at or near the point of sale, far earlier than traditional models. By leveraging real-time telematics—like driving behavior, mileage, and braking patterns—Lemonade can offer personalized pricing upfront, which management says has led to “conversion rates jump by over 60% in the past few months.” This early pricing precision helps attract the right customers (e.g., safe, younger drivers often overcharged by competitors) while setting the stage for better long-term underwriting outcomes.

On the cross-sell front, Lemonade has refined its bundling flows—streamlining how existing customers are pitched Car insurance alongside their other policies, like renters or pet. This includes smarter targeting, improved user experience in the app, and tailored marketing, resulting in “more than doubling our cross-sales volume year-over-year.”

However, challenges remain. Car’s loss ratio is elevated due to a young book, though “older cohorts are seasoning nicely,” with a “double-digit loss ratio improvement as new cohorts pass the renewal date.” CFO Timothy Bixby noted that retention rates are impacted by a “new business penalty,” but

at 6 months, we typically see something on the order of a double-digit 10%-ish improvement,

in both loss ratio and retention.

To track this segment’s health, I’m introducing my Proprietary Adjusted Rule of 40 for Car, summing IFP growth and (1 - Gross Loss Ratio). In Q1 2025, it scores a modest 21—well below the company-wide metric, which exceeds 40—reflecting early-stage challenges. Still, the trajectory is encouraging, and I’ll be watching for consistent improvement in this metric each quarter.

Lemonade Business Ontology

As I outlined in my deep dive, my framework for analyzing Lemonade centers on a Business Ontology that captures the company’s operational and strategic health through a few key lenses: growth, efficiency, and profitability. Growth is measured by in-force premium (IFP) and customer acquisition trends, reflecting Lemonade’s ability to scale its book of business. Efficiency is tracked via metrics like IFP per employee, which highlights how well the company leverages its tech-driven model to drive productivity. Profitability is assessed through the loss ratio and progress toward breakeven, gauging Lemonade’s path to sustainable margins. Additionally, I layer in retention metrics—such as annual dollar retention—to understand customer stickiness, a critical driver of long-term value in insurance. This ontology isn’t static; it evolves with Lemonade’s journey, especially as newer segments like Car gain prominence. By focusing on these pillars, I aim to cut through the noise and provide a clear, repeatable blueprint for evaluating Lemonade’s performance each quarter, ensuring we’re tracking what truly matters as the company scales.

If you’re new to my Business Ontology framework, check out this article for a detailed introduction.

Annual Dollar Retention

Lemonade’s Annual Dollar Retention (ADR), a key indicator of customer stickiness, came in at 84% in Q1 2025, down 4 percentage points from Q1 2024’s 88%, and slightly below the 86% reported in Q4 2024.

The decline is largely attributable to the non-renewal of policies which failed to meet certain underwriting criteria, as discussed in prior updates. CFO Timothy Bixby provided further color:

In broad strokes, we saw an unfavorable impact to ADR from our continuing effort to improve the profitability of our home book of about 4 points, about 2 points unfavorable from our pay-per-mile car product and about 2 points favorable from the rest of the book,

Despite the dip, I believe ADR is bottoming out around this level and expect it to rebound toward its prior peak of 88% over the next 3-4 quarters, especially as underwriting adjustments stabilize.

Retention should also get a boost from Lemonade’s cross-sell momentum. Bixby noted,

We saw more of our growth coming from cross-sells… our multi-policy rate is increasing, and we’re now heading towards almost 5% of our customers having multi-policy,

He added,

Something like half of our new sales are now coming—of car coming from existing customers,

up from a third historically, with a “deep pool” of 2.5 million non-Car customers to tap. As multi-policy adoption grows, retention is poised to improve, supporting a recovery in ADR and reinforcing the long-term value of Lemonade’s customer base.

IFP per Employee

Lemonade’s tech-driven efficiency continues to shine, as evidenced by its IFP per employee metric, a core gauge of operational leverage in my Business Ontology. In Q1 2025, IFP reached $1,008 millions, up 27% year-over-year, while headcount grew only 2% to 1,260 employees.

The chart below underscores this efficiency: over the past 10 quarters, IFP has surged 65%, while operating expenses excluding growth spend (OpEx ex. growth) remained nearly flat.

CEO Daniel Schreiber tied this to Lemonade’s AI core, stating,

When you see our top line surging by 2/3 even as fixed costs stay flat or fall, what you are seeing is AI hard at work… its power is increasingly apparent in our P&L,

This dynamic—leveraging AI to scale the book without proportional cost increases—positions Lemonade to widen its gross profit margins over time, a trend I expect to persist as the company continues to prioritize efficiency.

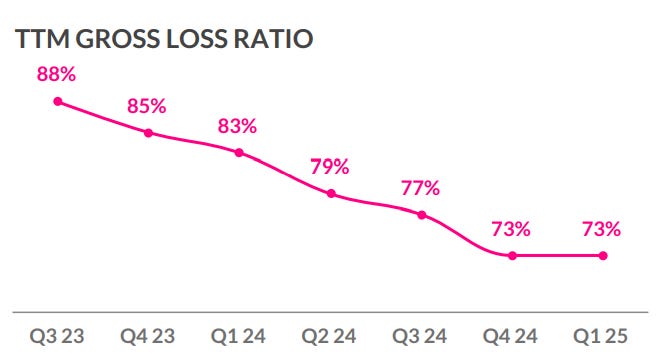

Loss Ratio

Lemonade’s underwriting performance in Q1 2025 remains on track, with the trailing twelve months (TTM) gross loss ratio steady at 73%, unchanged from Q4 2024.

However, as expected, the quarterly gross loss ratio was higher at 78%, impacted by the California Wildfires, which added as much as 16 points to the ratio.

My Proprietary Adjusted Rule of 40, which sums IFP growth and (1 - Net Loss Ratio) to help to visualize how Lemonade is balancing growth with profit, scored a solid 45 in Q1, still up YoY but down sequentially from 64 of Q4 2024. Again, this is because of the hit taken from the wildfires.

Adjusting for catastrophes (ex-CAT), the Rule of 40 improves to 68 signaling that the positive trend of this metric and its underlying meaning is likely going to continue over the next quarters.

This resilience, despite significant CAT events, underscores the company’s progress toward sustainable profitability, though continued focus on loss ratio stability will be key as the Car segment scales.

Conclusion

Lemonade’s Q1 2025 performance reinforces my conviction in this investment, with the core thesis—centered on AI-driven growth, efficiency, and a path to profitability—remaining firmly intact. The company continues to execute against its ambitious roadmap, delivering 27% IFP growth, a stable 73% TTM gross loss ratio despite wildfire impacts, and impressive operational leverage.

The Car segment, a critical growth engine, is gaining momentum with faster sequential IFP growth and improving cross-sell dynamics.

Management’s guidance further bolsters confidence:

Our IFP guidance reiterates FY IFP growth of 28% – sustained acceleration towards our cruising velocity of 30%, expected in 2026… We reiterate our guidance of positive Adj. FCF in 2025, despite the unfavorable impact of the California Wildfires in the first quarter,

With a clear trajectory toward 30% IFP growth, positive adjusted free cash flow this year, and a raised outlook for gross earned premium and revenue, Lemonade is on pace to deliver on its long-term vision. While challenges like ADR softness and Car’s early-stage loss ratio persist, the overall picture supports my bullish stance—Lemonade remains a compelling growth story with a disciplined path to profitability.

As always, here is the “Deep Dive To Date” (DDTD), that is how the stock is performing since my initial deep dive on the September 24th 2024, when the stock price was $17.23.

+80% DDTDSee you in the next update!

Check all the Ontologies I have built: ODD 0.00%↑ , RKLB 0.00%↑ , HIMS 0.00%↑ , DUOL 0.00%↑ , CRWD 0.00%↑.

The content of this analysis is for entertainment and informational purposes only and should not be considered financial or investment advice. Please conduct your own thorough research and due diligence before making any investment decisions and consult with a professional if needed.

Many thanks for the update. Many positives in the report, especially overall GLR and absorbing the hit from California wildfires. But also some unexpected bad news with Car and Europe GLR and in ADR.

In principle I can accept their new business penalty explanation because QoQ IFP growth in these products was significant. But still the explanation is quite generic and vague, and it makes modelling of next quarters more tricky.

So now we have to expect accelerated IFP growth to produce worse GLR and ADR… at least a few quarters, or longer? And by how much? And how to track this? Needs more adjusted metrics which is frustrating.

I see your frustration Olli. But look, Car is I believe less than 10% of the total IFP and also Europe doesn’t weight much. Before their GLR and ADR can really impact the total number I expect they will fix it (this is why they didn’t accelerate on Car sooner, they wanted to have GLR under control). From here, I expect to see the ADR bottoming this or next quarter and improving from there. IMO no need of major changes to the Business Ontology metrics, everything is on track.