Mercado Libre: the best time to buy

$MELI Q4 2025 ER Update

The content of this analysis is for entertainment and informational purposes only and should not be considered financial or investment advice. Please conduct your own thorough research and due diligence before making any investment decisions and consult with a professional if needed.

$MELI is, in my opinion, one of the most misunderstood large caps in the market right now.

It’s growing revenue ~40% YoY, it’s scaling logistics + fintech in a way no one else in LatAm can replicate, and yet it’s priced like a business that is about to die.

That mismatch is my thesis.

Table of Contents

Q4 2025 Update

Lorenzo2cents (L2C) take aways and performance

Business Ontology Framework by L2C

Business Ontology

4D Valuation Model

L2C portfolio strategy

Q4 2025 Update

I get why Mr. Market is nervous:

LatAm macro always feels “fragile” (FX, inflation, politics)

Competition is real (especially in Brazil)

When MELI invests aggressively, margins look worse in the short term

But here’s the key: these worries don’t explain the price.

If you price a company like it’s ex-growth, you better have evidence that the machine is breaking.

So let’s look at the machine.

Brazil: “go beast mode” worked

A few months ago MELI turned aggressive in Brazil. More subsidies, lower free shipping threshold, better value proposition.

This is the type of move that scares Wall Street, because it looks like “profitability sacrifice”.

But it’s not charity. It’s a land grab.

And it’s working.

Here’s how management framed it: the acceleration

is the result of our strategic investments to enhance the value proposition, most notably the decision to lower the free shipping threshold.

More free shipping

is driving higher purchase frequency and bringing new buyers into the ecosystem.

Then the key line:

This volume is translating directly into efficiency. Our logistics network absorbed the increase in volumes while driving productivity gains, proving our ability to scale effectively.

In numbers, that means:

GMV in Brazil +35% YoY

Sold items +45%

Logistics absorbed the volume while improving productivity

This is important: they didn’t just buy growth with dumb spending. They scaled.

When you can scale logistics efficiently, you build a moat.

Argentina: same playbook, bigger check

Now they’re doing something similar in Argentina.

On March 11, 2026, CEO Ariel Szarfsztejn announced a plan to invest $3.4B in Argentina in 2026 (roughly +30% vs 2025).

Where is the money going?

Logistics network (distribution centers)

E-commerce platform + tech

Fintech ecosystem (Mercado Pago)

Plus ~1,900–2,000 new hires.

Again: short term pain, long term dominance.

Think about it like this.

If you want to build the “Amazon + PayPal” of an entire continent, you don’t optimize for quarterly margins. You optimize for being unavoidable.

The profitability fear is overplayed

A lot of the bear case is basically: “competition will force higher marketing spend, and MELI will lose unit economics.”

But when you actually do the math, the opposite shows up.

If you approximate CAC payback as marketing spend divided by incremental gross profit (a rough but useful sanity check), it improved from ~13.2 months (2024) to ~11.8 months (2025).

Translation: MELI’s customer acquisition machine became more efficient, not less.

In a tougher environment.

That’s not what a company under structural pressure looks like.

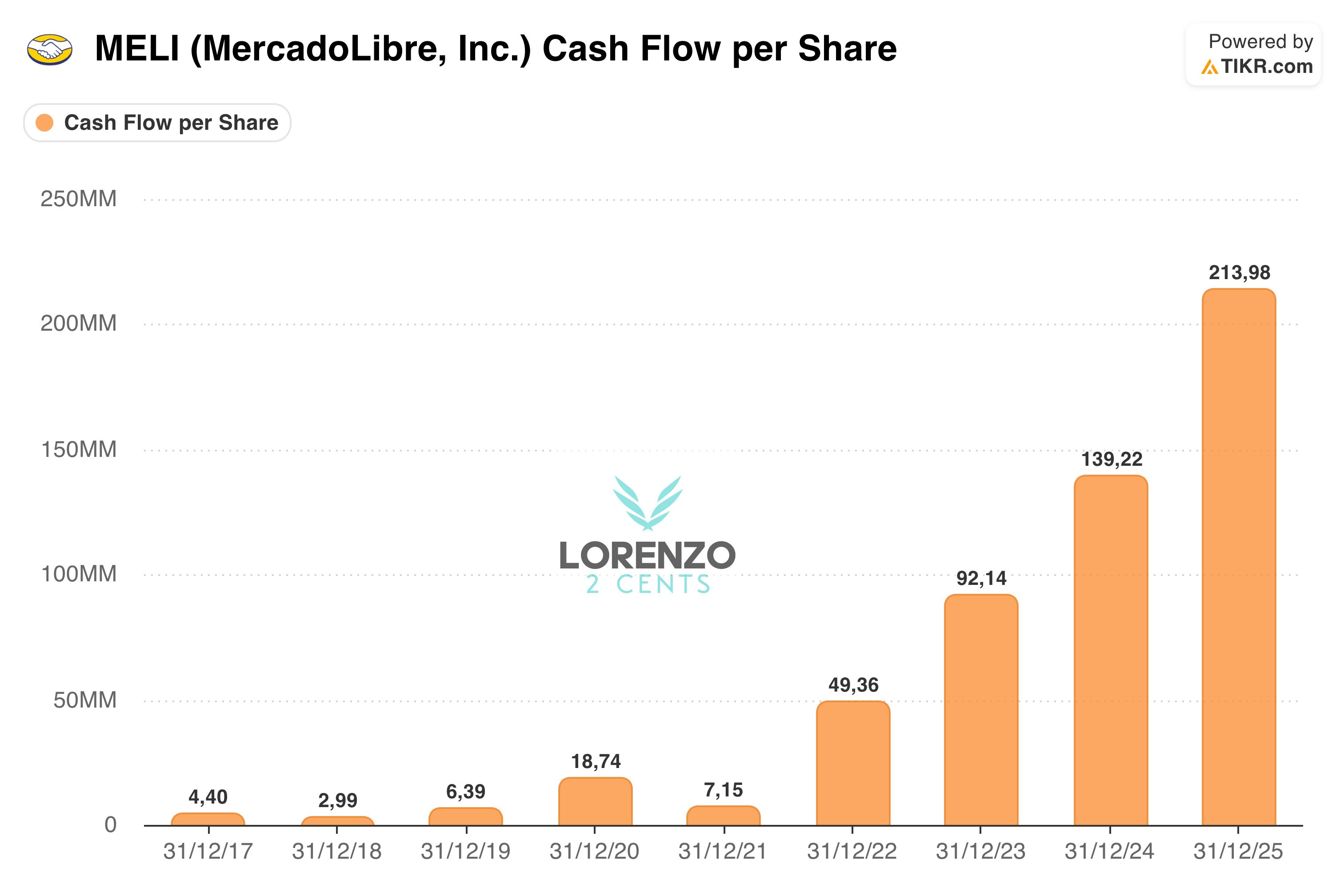

The proof that matters: FCF/share is compounding

At the end of the day, I don’t care about “narratives”. I care about whether the business is turning into cash for shareholders.

If MELI’s investments were reckless, you would see it in the per-share economics.

Instead, what you see (zoom out) is a pretty clean story: FCF/share keeps going up.

This is the single best rebuttal to the “they’re buying growth at any cost” argument.

The best time to buy is when price goes down while value goes up

$MELI is down ~17% YTD.

But the business is not deteriorating.

It’s strengthening.

This is a classic pattern:

management invests for long-term growth

margins compress a bit

Wall Street panics

stock sells off

long-term investors get a gift

I love when this happens, because it’s one of the few moments where you can buy quality at a discount.

“We’re not trying to optimize short-term margin” (and that’s exactly the point)

The CFO said it clearly during the earnings call:

their focus is capturing commerce, fintech, ads opportunities

they will invest even if it pressures margin short-term

they manage for the long term

If you’re an investor, that should not scare you.

It should make you ask a better question:

“What do they become if this strategy works?”

The next big bet: advertising

The next leg of the story is ads.

MELI sits on something extremely valuable: first-party data on real commerce behavior.

Not “likes” or “views”.

Actual intent.

If you believe in a world of agentic commerce (AI agents shopping for you), this becomes even more interesting.

Because:

shopping moves faster from offline to online

discovery becomes algorithmic

whoever owns the transaction graph owns the monetization

MELI is building its own agentic experience inside the platform (search, recommendations, discovery).

But there’s a second angle: off-platform advertising services, attribution, tech stack for third parties.

If commerce runs at low single-digit margins to win the market, fintech + ads can print money.

That’s the shape of the long-term MELI.

Lorenzo2cents (L2C) take aways and performance

The stock is priced like a problem.

The business looks like a compounding machine.

That’s why I think the best time to buy is when the market is focused on short-term margin noise, while MELI is building long-term dominance.

DYODD. I’m long-term bullish on $MELI.

As always, here is the “Deep Dive To Date” (DDTD), that is how the stock is performing since my initial deep dive on the May 18th 2025, when the stock price was $2585. As proved by my post on X, where I share real time updates, I opened a position a few days later.

- 35% DDTDFrom here on, the content is restricted to L2C Premium Members, folks who’ve chosen to unlock this toolkit and support my independent research:

Business Ontology Framework by L2C

Business Ontology: My core blueprint for modeling and tracking company performance at every level.

4D Valuation Model: the valuation tool I use to value all my investments (Fair price is useless)

L2C Portfolio Strategy: My portfolio allocation and strategy in details

L2C Portfolio access & trades alerts: Real-time views into my holdings, plus instant notifications on buys, sells, and shifts.

Business Ontology Framework by L2C

The Business Ontology is a framework I built after tearing apart several tech companies from the ground up—breaking them down to their basic parts and piecing together a real thesis on what drives them. Think of it as a map of a company’s soul. It’s a tight set of core indicators—tailored to each business—that show if it’s heading the right way, no matter what the stock price says. These aren’t your basic stats like P/E ratios or revenue bumps you grab from Yahoo Finance. They’re deeper, sharper, and linked straight to the thesis I’ve cooked up on how the company makes value and fights in its market.

The framework boils down to two big pieces:

The Business Ontology—This checks if the company’s worth buying into or hanging onto.

The 4D Valuation Model—This gives you a 4D roadmap to guide your own calls on how much to put in (allocation).

Now, let’s dive into MELI and this quarter’s update.

Business Ontology

Here’s a quick visual on the Business Ontology for MELI.