MercadoLibre: The Market Is Missing the Jevons Paradox

$MELI Q1 2026 ER Update

MercadoLibre reported another stellar quarter, and the market hated it.

Revenue grew 49% year over year to $8.8 billion, the fastest pace in almost four years. GMV grew 42% to $19.0 billion. TPV grew 50% to $87.2 billion. Fintech monthly active users reached 82,9 million, up 29% year over year. The credit portfolio reached $14.6 billion, up 87% year over year.

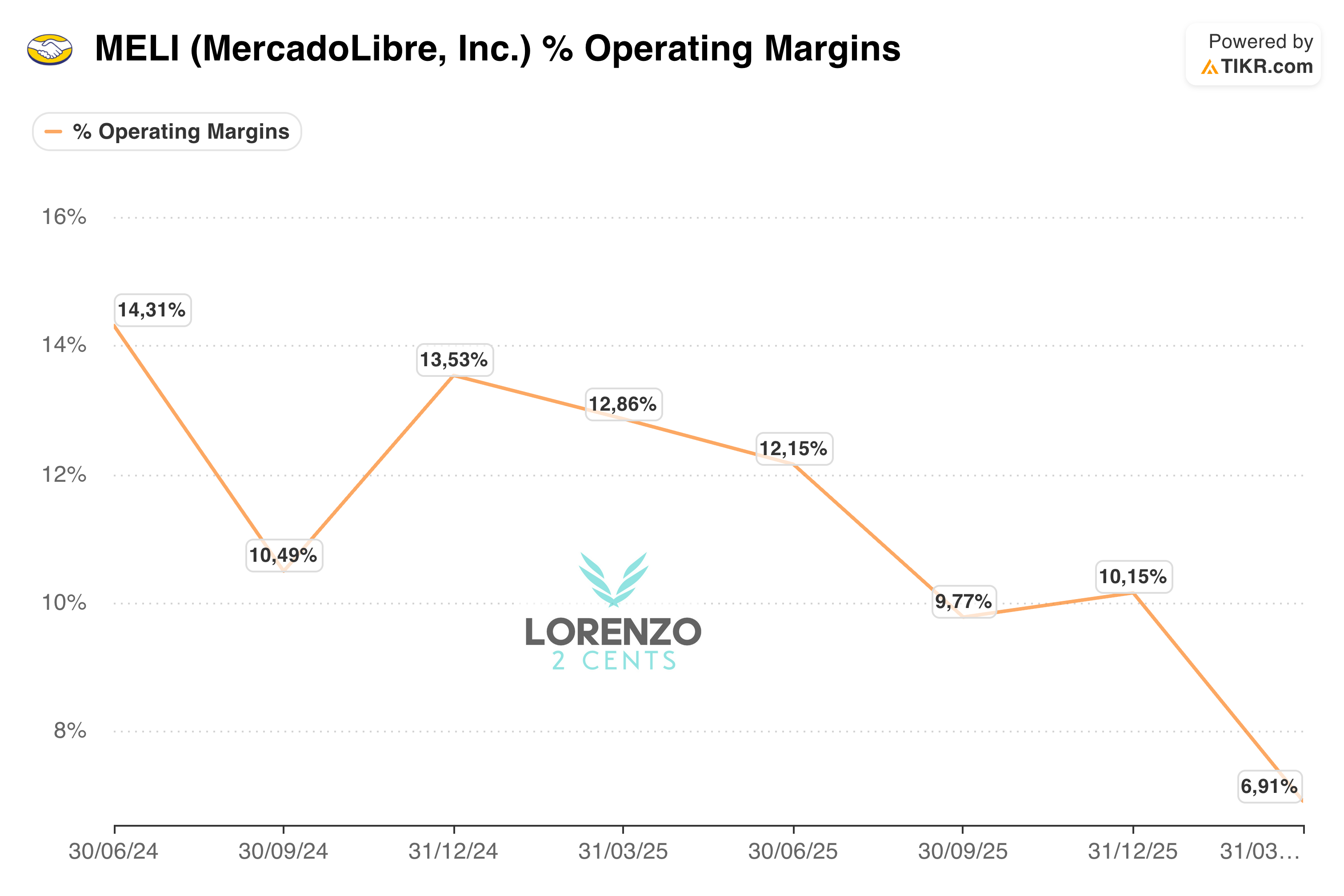

And yet the stock sold off because operating margin fell to 6.9%, down 600 basis points year over year.

But the headline is not that MercadoLibre is suddenly less profitable. The headline is that MercadoLibre is choosing to invest aggressively because the opportunity in front of it is still enormous, and those investments are already producing faster growth, stronger network effects, and better scale economics.

Here is how Ariel Szarfsztejn, CEO of Mercado Libre, described competition in Brazil.

Brazil is one of the most attractive e-commerce markets in the world. So it’s natural that it’s getting more and more intense and as that has been the case for many years... competitive intensity is also having a positive impact in the market as a whole by bringing new consumers from the offline world into the online world, and we feel we are very much equipped to offer all those consumers the opportunity to buy in MercadoLibre. So the pie is increasing at a faster pace than it was before, and we are taking an even larger slice of that pie.

This sounds almost like a Jevons paradox.

In the original Jevons paradox, when something becomes more efficient, people do not necessarily consume less of it. They often consume more because the lower cost expands the total market.

Something similar is happening in Latin American e-commerce.

Competition, free shipping, better logistics, lower friction, better search, and better prices are not simply taking share from MercadoLibre. They are accelerating the migration from offline retail to online retail. And when more consumers move online, MercadoLibre is structurally advantaged because it has the largest marketplace, the strongest logistics network, the most trusted payments layer, and the best data loop in the region.

In other words, competition is not necessarily a zero-sum game yet.

Latin America is still too early.

Management reminded investors that the average American makes 41 online purchases per year, while the average Latin American makes just 7. MercadoLibre buyers average 11. That gap is the whole thesis.

If the market grows faster because consumers are being pulled online more aggressively, the largest platform can benefit even if the environment looks more competitive on the surface.

That is exactly what Q1 showed.

Brazil: The Flywheel Is Working

Brazil was the standout market again.

MercadoLibre lowered the free shipping threshold in Brazil in 2025, and the market initially interpreted it as a margin-negative competitive response. But the data keeps pointing in the opposite direction: it is a long-term investment that is expanding the market, increasing frequency, and improving the utilization of MercadoLibre’s infrastructure.

Management put it clearly:

By bringing more buyers into the ecosystem, we’re strengthening network effects with higher purchase frequency, broader assortment and a logistics network that becomes more efficient with every incremental package. As a result, Brazil delivered another standout quarter for commerce. GMV grew 38% year-over-year as items sold growth accelerated to 56%. This is more than double the quarterly growth rate prior to lowering the free shipping threshold.

Free shipping penetration reached a new record and unit economics continue to improve with cost per shipment down 17% year-over-year in local currency. In other words, higher demand is driving lower costs.

This is the core point.

More demand is not just more revenue. More demand means more packages through the same network. More packages improve route density, fulfillment utilization, line-haul efficiency, and last-mile economics. MercadoLibre already has the most advanced logistics infrastructure in the region, so incremental volume should improve the economics of the network over time.

This is why I think the market is misreading the margin compression.

If the lower free shipping threshold were simply a price cut with no strategic benefit, I would be worried. But if it brings more buyers into the ecosystem, increases frequency, expands category breadth, improves logistics density, and strengthens the marketplace, then the short-term margin hit is an investment.

And the investment is clearly working.

Brazil GMV grew 38% FX-neutral. Items sold grew 56%. Unique buyer growth accelerated to 32%, the fastest pace in five years. Unit shipping costs in Brazil fell 17% year over year in local currency.

The market sees lower margins. I see MercadoLibre pulling more of Latin America into its ecosystem.

The impact of AI Is Still Underappreciated

Another part of the quarter that I think is still underappreciated is AI.

Most investors do not think of MercadoLibre as an AI beneficiary. They think about marketplace, logistics, payments, credit, and maybe ads. But AI directly improves the economics of all of these layers.

Management said:

We deployed LLMs in search in commerce for the first time this quarter. And basically, that is live in Brazil, Mexico and Argentina. So now we are using this technology to better understand users’ intent, combining both knowledge on the user behind the query and better interpretation of the query itself. And the impact is basically very visible across the funnel. We have higher conversions as buyers find what they are looking for much faster.

We have better ad returns as our search also improves the quality of the results that our ad tech stack is generating. We have higher -- stronger engagement from our users as the discovery experience actually improves. And clearly, this is one of the contributors to the great performance we had this quarter.

This matters because MercadoLibre has one of the richest first-party datasets in Latin America: shopping intent, payment behavior, merchant data, credit performance, logistics data, search data, and advertising performance.

LLMs improve the search layer, but the impact does not stop there.

Better search means higher conversion. Higher conversion means more GMV. More GMV means more payment volume. More payment volume means more data. More data improves underwriting, ads targeting, and personalization. Better personalization increases engagement. Higher engagement increases frequency.

That is the ecosystem loop.

The low-hanging fruit is advertising. If AI improves search relevance and sponsored listing performance, ad ROI improves. When ad ROI improves, sellers can spend more. MercadoLibre said ads revenue grew 73% in USD and 63% FX-neutral in Q1.

MELI does not disclose Mercado Ads revenue as a separate line item, but based on prior disclosed ads penetration and Q1’26 growth, Mercado Ads was likely running at roughly $2B annualized run-rate.

This is still a small line relative to the full business, but it is a structurally high-margin opportunity. It also reinforces the marketplace, because better ads help sellers sell more and help buyers discover more relevant products.

But I think the bigger AI opportunity is not only ads. It is the improvement of the entire consumer experience. Search becomes more natural. Discovery becomes better. Credit decisions become more precise. Customer support becomes cheaper. Logistics workflows become more productive. Seller tools become more useful.

This is not an AI story in the hype sense. It is an AI story because MercadoLibre has scale, proprietary data, distribution, and real use cases.

The Margin Compression Is Not What It Looks Like

The main reason the stock is trading around 2.5x LTM revenue is that investors are worried about competition and margin pressure.

I understand the concern, but I think the conclusion is wrong.

MercadoLibre is not losing control of its business. It is deliberately choosing to invest because the returns on those investments are attractive.

Martin de los Santos, CFO at Mercado Libre, said it directly:

If we wanted to improve margins in the short term, it will be fairly easy for us to slow down certain investments, but we don’t think it’s the right way to go given the large opportunity that we have in front of us for both commerce and fintech.

This is not a management team trying to explain away a broken model. This is a management team saying: we can harvest, but harvesting would be the wrong capital allocation decision.

The biggest distortion is in Mercado Pago.

The credit book grew 87% year over year, much faster than consolidated revenue growth of 49%. That creates accounting margin pressure because MercadoLibre has to provision expected losses upfront when it originates new credit.

Management explained the mechanics:

The fact that our credit book grows at a faster pace than revenues, the credit book grows at 87% year-on-year and our revenues for MercadoLibre growth at 49%, that generates margin compression.

And the reason for that is because as we issue any new loan, we have to provision for the full amount of the expected loss of that loan. And when we accelerate growth, we need to provision more.

So 2/3 of the margin compression comes from that.

This is crucial.

If the credit book is growing profitably, then near-term provisions are not the same thing as structural margin deterioration. They are the accounting cost of growth.

MercadoLibre’s Q1 NIMAL was 17.8%, down from 22.7% a year ago, mainly because of the higher mix of lower-spread credit cards and some spread compression in Brazil. That decline is worth watching. But 17.8% NIMAL is still an extremely attractive return profile, especially if the credit book is expanding and asset quality remains controlled.

The 15-90 day NPL ratio was 8.0%, broadly stable year over year, according to the company. Management also said that each of its consumer and merchant loan portfolios remains highly profitable.

So I do not think the right conclusion is “Mercado Pago is destroying margins.”

The right conclusion is: Mercado Pago is growing so fast that the accounting cost of new credit is temporarily compressing margins, while the future earnings power of the credit book is being built.

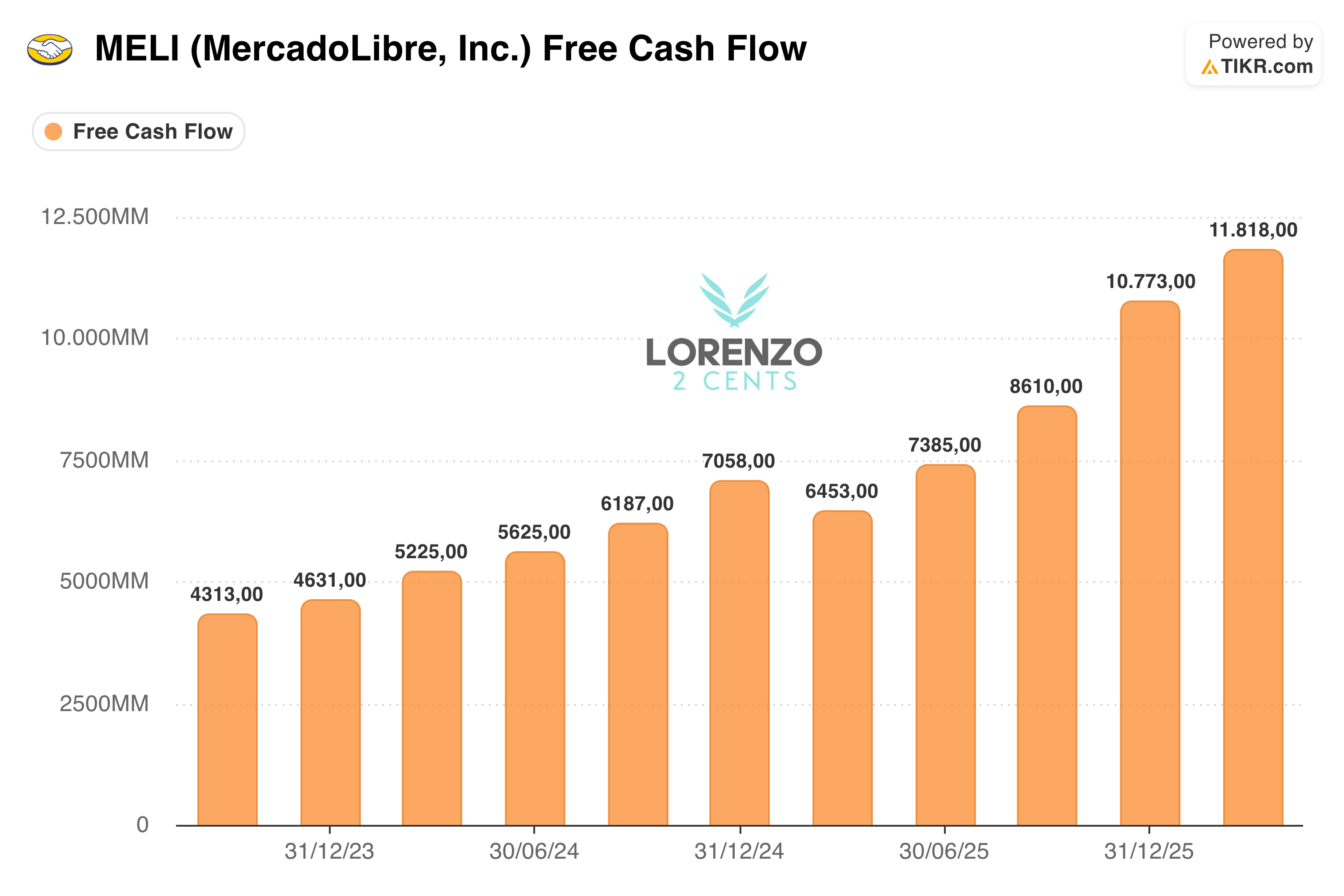

FCF: Do Not Treat Loan Growth Like a Cost

This is also why I think the way we calculate free cash flow matters.

If we subtract all cash used to grow the loan book as if it were an operating cost, as per standard account practice and as often done by investors, we risk dramatically understating the value of MercadoLibre.

That cash is not being burned. It is being converted into financial assets that generate yield.

Using the standard free cash flow definition:

Free Cash Flow = Cash From Operations - Capex

MercadoLibre generated roughly $11.8 billion of LTM free cash flow through Q1 2026 (LTM):

That is the number I care about for the main valuation framework.

Yes, the credit book requires capital. Yes, provisions and funding costs matter. Yes, NPLs must be watched carefully. But deducting loan originations 1:1 from FCF can make the business look much less valuable than it is, because it treats a productive asset like a cost.

The right way to think about it, in my opinion, is to keep reported FCF as the main line and analyze credit-book growth separately: NIMAL, NPLs, funding costs, portfolio mix, and return on the capital deployed.

If those metrics deteriorate, then the thesis changes. But as of Q1, I do not see evidence that MercadoLibre is simply buying growth with bad credit.

I see a company investing aggressively into a credit opportunity where it has unique data, distribution, and ecosystem advantages.

Mercado Pago vs Nubank: The Business Ontology Test

One of the most important data points I am watching for my Business Ontology is the performance of Mercado Pago versus Nubank.

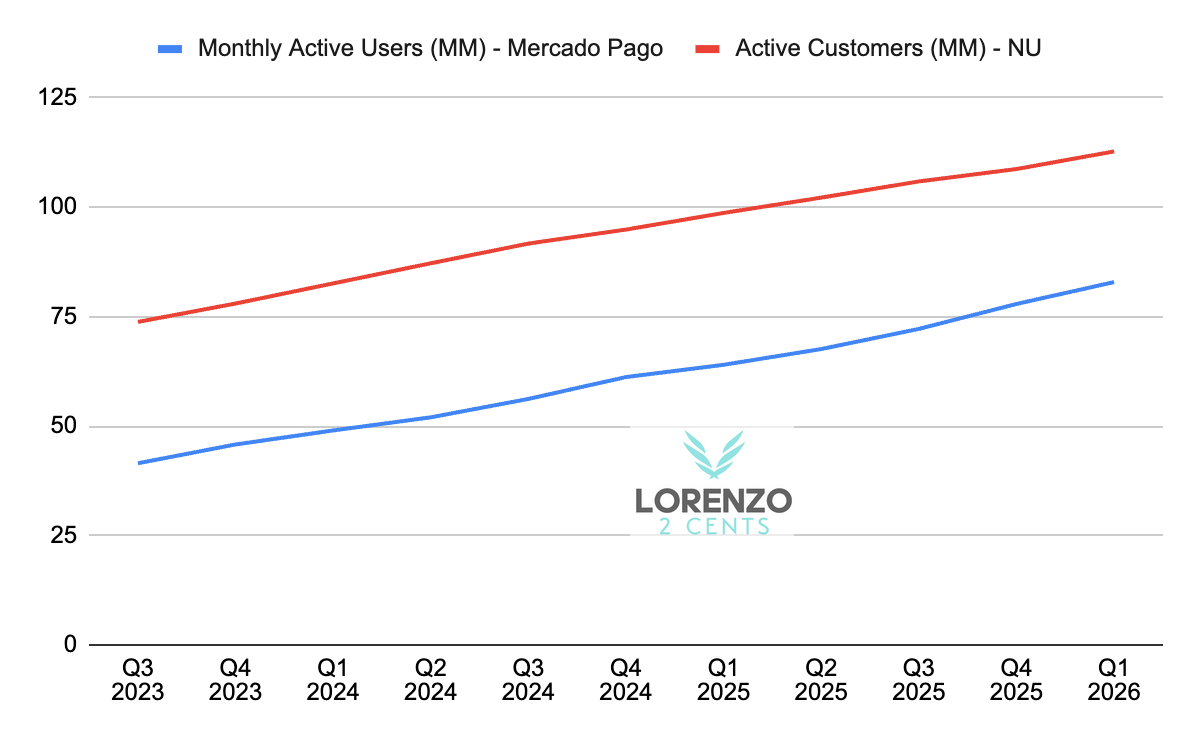

Nubank is probably the cleanest benchmark for Latin American fintech at scale. It is an incredible business. It has more than 135 million customers, a monthly activity rate of 83%, and a credit portfolio of $37.2 billion, up 40% year over year FXN.

But Mercado Pago is becoming harder to ignore.

Mercado Pago reached 82,9 million monthly active users, up 29% year over year.

Its credit portfolio reached $14.6 billion, up 87% year over year. AUM reached almost $20 billion, up 77% year over year.

The active-user comparison is also interesting. Nubank had more than 135 million customers in Q1 2026 and an 83% monthly activity rate, which implies roughly 112 million active customers. That is still larger than Mercado Pago, but Nubank’s active base grew from 98.7 million monthly active users in Q1 2025 to roughly 112 million in Q1 2026, or about 14%. Mercado Pago’s active user base grew 29% over the same period.

The profitability of credit also tells a more nuanced story. Nubank’s risk-adjusted NIM was 9.5% in Q1 2026, down from 10.5% in Q4 2025. Mercado Pago’s NIMAL was 17.8%, down from 22.7% a year ago. These are not perfectly identical metrics, so I would not overstate the comparison. But directionally, Mercado Pago is scaling credit faster, with a higher reported credit spread, while Nubank remains the larger and more mature fintech machine.

So Nubank is still much larger in credit portfolio and active customer scale. But Mercado Pago is growing active users and credit faster, and it is doing it from inside the MercadoLibre ecosystem.

This is exactly my thesis.

The combination of commerce + fintech should create advantages that a standalone digital bank does not fully replicate.

MercadoLibre knows what consumers buy, what merchants sell, how often they transact, what categories they participate in, how payments flow, how logistics behave, and how users interact across the platform. This gives Mercado Pago a different underwriting and distribution advantage.

A standalone fintech can have an excellent app and an excellent brand. Mercado Pago has that too, but it also has the marketplace.

MercadoLibre is not just a marketplace with a payment app. It is a commerce and financial infrastructure layer for Latin America.

What Could Re-rate the Stock?

I do not think a re-rate is imminent. The market is clearly skeptical, and investors usually do not reward margin compression until they can see stabilization.

But a few catalysts could change the narrative.

First, a stock split. Economically, it changes nothing. But MELI’s share price is high, and a split could renew retail investor interest, especially if the fundamental story is already improving.

Second, NIMAL stabilization. The decline from 22.7% to 17.8% is one of the concerns. If NIMAL stabilizes while the credit book keeps growing, the market may start seeing the credit investment as value creation rather than margin risk.

Third, margin stabilization. Management does not need to maximize margins today, but investors need evidence that margins are being compressed by choice, not by necessity.

Fourth, continued FCF growth. If free cash flow per share keeps rising while the company reinvests aggressively, the market will eventually have to reconcile the narrative of margin pressure with the reality of cash generation.

Fifth, capital rotation from AI stocks. MercadoLibre is not an obvious AI trade, but it is one of the few large-cap businesses where AI can improve an already dominant marketplace/fintech ecosystem. If investors start looking for non-obvious AI beneficiaries with real earnings and real data advantages, MELI fits that bucket.

L2C take aways and performance

MercadoLibre is being priced like a company whose margins are under attack.

I think it is a company choosing to reinvest at high rates because the opportunity is still underpenetrated, and because its ecosystem advantages are getting stronger.

Q1 2026 was not a clean quarter if you only care about near-term EPS. Operating income declined, net income declined, and margins compressed.

But if you care about long-term value creation, the quarter was extremely strong.

Revenue growth accelerated. Brazil commerce accelerated. Items sold exploded. Logistics unit costs improved. Ads grew rapidly. Fintech MAUs grew. AUM grew. The credit portfolio expanded. AI started to show real business impact. Free cash flow remains very strong on an LTM basis.

The market sees lower margins.

I see a dominant platform with a huge volume of high quality first-party data investing to make the market bigger, take a larger slice of it, and turn that scale into long-term cash flow.

At roughly 2.5x LTM revenue, the asymmetry is becoming more and more interesting.

I do not know when the market will re-rate MELI. It may take time. But even without multiple expansion, a business compounding revenue and cash flow at these rates can still create significant value.

And if the market eventually understands that the margin compression is mostly a reinvestment cycle rather than structural damage, the upside could be much larger.

I am willing to wait.

I will soon publish a video where I explain my updated Rocket Lab 4D valuation model and the assumptions behind it.

If you want access to:

My portfolio

all my trades in real time

my price targets and how I calculate them

Business Ontology content

My price targets will be shared in the Telegram Group and explained on my Youtube channel.

I share my thoughts on X.

As always, here is the “Deep Dive To Date” (DDTD), that is how the stock is performing since my initial deep dive on the May 18th 2025, when the stock price was $2585. As proved by my post on X, where I share real time updates, I opened a position a few days later.

- 37% DDTDPlease note that:

I can be and will be (hopefully not often) WRONG. This is just my personal strategy—NOT FINANCIAL ADVICE. I don’t know your financial or life situation well enough to give any recommendations. Please do your own due diligence and research. Don’t be LAZY.

Be the architect of your own destiny.

Ciao

Lorenzo