Oddity: The Smartest Trade of All Time

$ODD Q4 2025 ER Update

The content of this analysis is for entertainment and informational purposes only and should not be considered financial or investment advice. Please conduct your own thorough research and due diligence before making any investment decisions and consult with a professional if needed.

Oddity fell off a cliff in Q4. On February 25, 2026, they announced record 2025 results—revenue up 25% to $810M with strong profitability—but warned of a sharp disruption in ad costs from an algorithm change at their largest advertising partner (likely Meta). This caused unprofitably high customer acquisition costs, leading to an expected ~30% revenue drop in Q1 2026, no full-year guidance, and the stock plummeting more than 50%.

Permabears couldn’t have asked for a better opportunity, and the narrative that Oddity is a scam came back stronger than ever.

Table of Contents

Q4 2025 Update

Lorenzo2cents (L2C) take aways and performance

Business Ontology Framework by L2C

Business Ontology

4D Valuation Model

L2C portfolio strategy

Q4 2025 Update

At the current share price, the company is a bargain unless you think it’s going out of business.

There are two valid arguments supporting the “out of business” thesis:

1 — Loss of trust in management, which isn’t telling the truth about what happened and is probably hiding something even worse than what they’ve shared

2 — The company can’t return to its previous growth rate and will actually lose market share as revenue continues to fall

My thoughts on point one are simple: I can’t see what could be worse than this. Oran (the CEO) presented the worst possible situation, saying they don’t even know how to fix it yet. What could be worse? He could have sugar-coated it, claiming they have a clear recovery plan and will return to growth quickly. In my view, he was fully transparent.

To the second point: Let’s dig deeper into what the issue is likely about.

The Issue

The issue Oddity faced stemmed from their unique “Try Before You Buy” (TBYB) model on IL Makiage (and SpoiledChild), which lets customers pay only shipping upfront for a trial, then keep/pay or return the product.

This model boosts conversions and reduces buyer risk (mimicking in-store trying), driving strong growth and high repeat rates (~70% of revenue from repeats). However, it has inherently higher return rates compared to standard e-commerce beauty purchases.

The company’s largest advertising partner (widely interpreted as Meta—Facebook/Instagram, based on analyst notes and context) recently updated its algorithms. The new algo began interpreting TBYB-related signals (especially elevated returns) negatively:

It viewed these as lower-quality or riskier signals (e.g., higher post-purchase dissatisfaction indicators).

This diverted Oddity’s ad campaigns into lower-quality auctions with abnormally inflated costs (disconnected from market norms).

Result: Sharp spike in new user acquisition costs (CAC/CPA), making first-order profitability unsustainable at scale.

Oddity described this as an “unprecedented dislocation” and an “edge case” because TBYB is rare in beauty (most competitors avoid it due to logistics/complexity). They first noticed issues in H2 2025 (mentioned in prior calls), but it worsened sharply into early 2026.

They believe it’s fixable without ditching TBYB—through adjustments like infrastructure tweaks, better signal optimization, or platform workarounds—expecting meaningful progress in Q2 2026 and normalization in H2. They didn’t abandon the model, viewing it as a core pro-consumer differentiator.

In short: The algo change penalized their high-return TBYB setup → CAC explosion → scaled-back ad spend → ~30% Q1 2026 revenue drop expected.

Will Oddity Go Out of Business?

The question is: How long will it take the company to return to growth, and will 20%+ growth be restored or lost forever?

Nobody knows, of course, but here’s my speculation. I believe 2026 is a lost year, likely ending with 0% revenue growth or slightly negative YoY. The worst will be over in one month from now. The worst-case scenario is that they’ll need to ditch TBYB advertising, which will surely impact growth and/or profitability (to grow at the same rate, they’ll bear higher CAC).

In 2027, Oddity will resume double-digit growth. It’s unclear whether they’ll return to 20%+.

Lorenzo2cents (L2C) take aways and performance

Oddity is clearly fragile right now, depending on Meta for survival, which isn’t sustainable long-term. I’d argue this event will end up making them stronger, forcing them to diversify ad partners and channels. In the long term, this event could even be considered positive.

What happened helped me better understand how hard it is to build a Direct-to-Consumer business and the level of moat that D2C companies like Oddity, Lemonade, Duolingo and Hims have built by reaching scale and profitability.

Their race is against incumbents, not new entrants, and it’s unlikely any new player can achieve anything similar.

This also highlights how social network companies like Meta act as formidable gatekeepers, effectively collecting a commission on revenue from any company selling to consumers.

My Thesis

If the company doesn’t go out of business—which I don’t think it will—my thesis is unchanged, though it will likely take a bit longer to materialize.

The early signals for the newly launched brand, Methodiq, are encouraging as shared by management, backed up by TrustPilot and App Store reviews—4.6 and 4.2 respectively, with already 101 reviews on the former.

Oran mentioned that they’ve expanded their capabilities in peptides:

We recently expanded our capabilities into peptides to add to our small molecule foundations, and are working on peptide solutions in areas like acne and aging. This expansion into peptides gives us flexibility to identify the right modality to address an individual biological target.

At the same time, they’re working in parallel to improve topical delivery of different actives to ensure they reach the relevant areas in the skin and maximize the biological effect. They expect to have 8 products in market in 2026 made with ODDITY Labs molecules, including molecules that cover key categories like acne, eczema, and hyperpigmentation.

And more to come in the future that we are bullish about.

The Smartest Trade of All Time (NO FINANCIAL ADVICE)

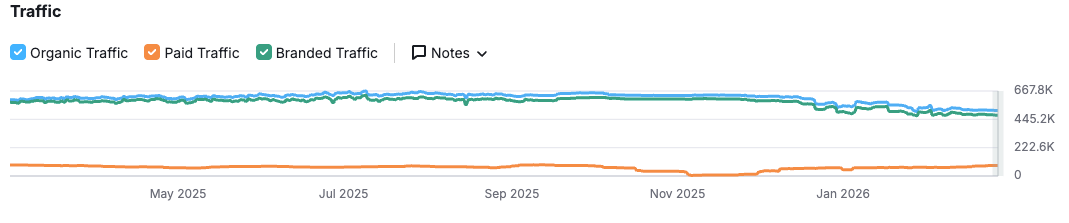

Looking at the web traffic of IlMakiage.com—the website of the brand that accounts for 70% of revenue—we can see a sharp decline starting in December, approximately when the issue became serious. The drop is about 30% from the high in September.

Web traffic is a proxy, and it likely lags the performance of ads by a few days or weeks, as it relates to organic traffic and (I don’t think) accounts for Meta ads direct traffic. Still, it should indirectly give a good indication of whether the situation has normalized. My guess is that web traffic will trend up before management announces normalization, as they’ll take their time to ensure it’s stable.

Since the company is basically trading at a ridiculous share price, any outcome other than bankruptcy will reprice it meaningfully higher. Being able to anticipate management’s announcement—even by one day—means we have a meaningful advantage.

As always, here is the “Deep Dive To Date” (DDTD), that is how the stock is performing since my initial deep dive on the July 16th 2024, when the price was $44.24.

-72%% DDTDFrom here on, the content is restricted to L2C Premium Members, folks who’ve chosen to unlock this toolkit and support my independent research:

Business Ontology Framework by L2C

Business Ontology: My core blueprint for modeling and tracking company performance at every level.

4D Valuation Model: the valuation tool I use to value all my investments (Fair price is useless)

L2C Portfolio Strategy: My portfolio allocation and strategy in details

L2C Portfolio access & trades alerts: Real-time views into my holdings, plus instant notifications on buys, sells, and shifts.

Business Ontology Framework by L2C

The Business Ontology is a framework I built after tearing apart several tech companies from the ground up—breaking them down to their basic parts and piecing together a real thesis on what drives them. Think of it as a map of a company’s soul. It’s a tight set of core indicators—tailored to each business—that show if it’s heading the right way, no matter what the stock price says. These aren’t your basic stats like P/E ratios or revenue bumps you grab from Yahoo Finance. They’re deeper, sharper, and linked straight to the thesis I’ve cooked up on how the company makes value and fights in its market.

The framework boils down to two big pieces:

The Business Ontology—This checks if the company’s worth buying into or hanging onto.

The 4D Valuation Model—This gives you a 4D roadmap to guide your own calls on how much to put in (allocation).

Now, let’s dive into Lemonade and this quarter’s update.