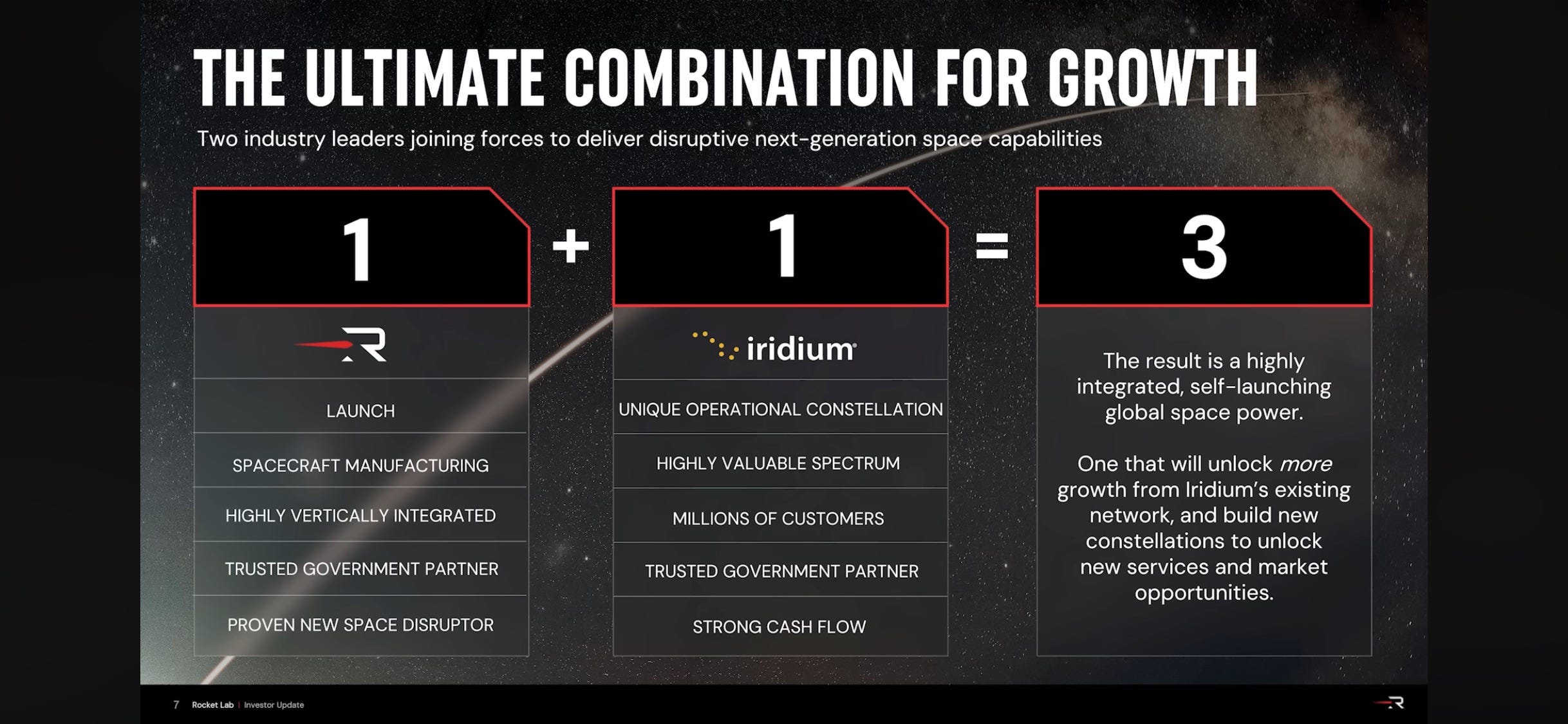

What Iridium Acquisition Means For Rocket Lab

Buying what cannot be easily built

Rocket Lab already knows how to build rockets, satellites, solar panels, payloads and components. With Neutron, it also wants to launch complete constellations at scale.

But manufacturing and launching satellites is not the same as operating a global constellation service.

Rocket Lab is buying what cannot be easily built.

Iridium brings:

scarce, globally coordinated spectrum;

a constellation operating continuously across the entire planet;

government, aviation and maritime certifications;

more than 500 commercial and technology partners;

billing, provisioning and customer-support infrastructure;

decades of experience managing a mission-critical satellite network;

recurring cash flow that can help finance the next constellation and reduce future dilution.

These capabilities would take Rocket Lab many years to reproduce—and some, particularly the spectrum and regulatory rights, might be impossible to replicate.

This is what Rocket Lab is really buying.

In this article, I’ll share my first thoughts and considerations following Rocket Lab’s latest acquisition.

The Business Opportunity for Iridium’s Constellation

These are the numbers for Iridium’s current business:

Total Revenue (Q1 2026): $219.1 million (+2% YoY)

Service Revenue (recurring, 72% of total): $158.0 million (+2% YoY)

And these are the lines of business that make up its revenue:

Commercial Service $130.4 million +2% ~60% Largest segment. IoT is the main growth driver (+5%). Voice & Data stable with pricing gains. Government Service $27.6 million +3% ~13% Stable, driven by EMSS contract with U.S. DoD. Equipment Sales $20.2 million -13% ~9% Down due to timing; expected flat for full year.

Engineering & Support Services $40.8 million +9% ~19% Growing, mostly U.S. government work.

Most of the current business comes from legacy areas, such as commercial voice and data and commercial broadband, which will likely shrink over time or grow only moderately.

The most promising area may be commercial IoT data. One might think that, with the explosion of drones and autonomous vehicles more broadly, this business could see strong growth. Every autonomous object will need to be tracked, and Iridium’s PNT (Positioning, Navigation and Timing) service is state of the art in terms of reliability. Thanks to its LEO positioning and Iridium’s unique spectrum, its signal is stronger, more robust and more reliable than GPS, although less accurate. It is normally used together with GPS in missions where PNT complements and protects GPS and other GNSS-reliant systems. In some situations, these systems can be put out of service by bad weather or hostile interference—in war and defense missions, for instance. In those cases, having a more reliable, although less accurate, positioning system becomes crucial.

Digging further into this topic, I discovered that even drones currently used in defense are not generally equipped with Iridium PNT or any equivalent service. When GPS is unavailable, they rely only on vision to navigate. This makes me less certain about the strategic importance and utility of Iridium PNT for most autonomous vehicles, and therefore less bullish about possible future hypergrowth in this line of business. However, the miniature application-specific integrated circuit (ASIC) Iridium is about to launch will allow partners to integrate its PNT services more cost-effectively, using less power and space.

That could make the service more compelling for autonomous vehicles.

The most promising business appears to be commercial IoT. Once Iridium launches its Direct-to-Device IoT connectivity later this year, every phone could potentially connect to Iridium satellites and use their services without needing additional hardware. It will also become easier and cheaper to integrate Iridium services into any IoT object, simply by using a small commercial modem. This will certainly boost IoT segment revenue. Until now, Iridium IoT required a dedicated receiver, making it complex and expensive—and, in some cases, simply not feasible.

Yet I am not convinced that this will be a game changer capable of turning Iridium into a hypergrowth story. For mobile phones, Iridium is a good solution for providing connectivity globally and in almost any weather condition. In that respect, it is more reliable than Starlink, which can struggle in bad weather despite offering broadband internet speeds, while Iridium can provide only the lower speeds needed for messages and phone calls. The question is: how large is this market? Even assuming that every phone maker in the world adopts it across its devices, the ARPU would probably remain tiny, although the service itself would still be compelling.

My conclusion—possibly wrong, since I have only just started analysing the topic and there is still a lot I do not know—is that current’s Iridium constellation is a stable, recurring-revenue business heavily weighted toward commercial IoT and government contracts. Growth is modest, in the low single digits, but reliable, with upside from new services such as D2D, PNT and aviation. It is not a high-growth company yet, but the Rocket Lab acquisition could accelerate its future expansion.

The biggest opportunity is still defense

If we look at who is launching things into space as a proxy of the space TAM share, there are four meaningful demand categories:

Communications constellations — largest volume, but overwhelmingly Starlink.

Defense and sovereign infrastructure — broadest and most dependable launch market.

Earth-observation intelligence — smaller satellites, recurring replenishment and growing defense demand.

Science, exploration and human spaceflight — valuable but government-funded and relatively slow-growing.

If we exclude Starlink, the most meaningful missions are funded directly or indirectly by governments.

For me, defense remains for Rocket Lab the clearest space hypergrowth opportunity for at least the next five years.

The US and its allies are moving from a few expensive satellites toward proliferated constellations for missile tracking, secure communications, intelligence, resilient navigation and space-domain awareness.

Rocket Lab was already moving in this direction. Its Space Development Agency contracts proved that it can compete for awards historically reserved for legacy aerospace primes.

Iridium reinforces the thesis.

The combined company can potentially offer a government the complete architecture:

Design the satellites. Build the payloads. Launch the constellation. Operate the network. Deliver the service.

That is a much stronger proposition than being only a launch provider or component supplier. Rocket Lab can take responsibility for the entire mission—and capture more of its economics.

Iridium also gives Rocket Lab something especially valuable in defense: operational credibility. It has already demonstrated that it can run a secure, resilient global constellation relied upon by governments and safety-critical industries.

Becoming a Platform: The AWS of Space

A customer planning a new constellation does not only need spacecraft. It needs network architecture, spectrum strategy, ground infrastructure, fleet management, continuous operations and distribution.

After Iridium, Rocket Lab can credibly sell a much broader outcome:

Rocket Lab will design, manufacture, launch and operate your constellation.

That positions Rocket Lab to compete as a prime contractor for commercial deals, while creating more opportunities to sell its own solar arrays, star trackers, reaction wheels, flight software, payloads and launch services.

Once a space company owns the complete stack, I would argue that it becomes a platform.

If you need to send assets into space and operate them there—especially as part of a constellation—you will probably standardize your payloads around Rocket Lab or SpaceX. Once you know how to design and build them for, say, Rocket Lab, you can standardize dimensions, processes, communication protocols and operations around the same provider.

This is what happened with cloud providers such as AWS. Once it became clear that running software in the cloud was cheaper, more reliable and more convenient than hosting it on-premise, software vendors and end-users began standardizing their operations around AWS, Azure or Google Cloud. In space, this dynamic could be even stronger because there is no real “on-premise” option. The choice is between rebuilding the entire stack from scratch every time or standardizing around one of the only two or three end-to-end space companies.

With this acquisition, Rocket Lab has everything required to become a platform—the same concept I described in my original deep dive. I think we are getting closer to seeing it become a reality.

The optionality is real—but not yet the thesis

Iridium mentioned several possible new services in its 2025 annual report, including aviation data through Aireon and Project Authentic, which aims to use Iridium’s PNT signal to authenticate the physical location of devices involved in sensitive transactions.

Project Authentic is interesting because it could move Iridium from backup navigation into cybersecurity. But it is still early: no named platform partners or commercial contracts have been disclosed.

I would treat these services as optionality, not as justification for paying $8 billion today.

Rocket Lab next constellation

As a simple way to see it, most launches today and in the future will be about one of three things:

Connecting things (internet, phones, IoT, drones)

Watching things (Earth, weather, military targets)

Enabling future ambitions (Moon bases, Mars, space industry)

SpaceX is capturing most of the connectivity business through Starlink, while IoT remains a smaller and slower-growing segment.

When it comes to future ambitions, I think Rocket Lab will play an important role in orbital data centers, even though this opportunity may not become viable or meaningful for at least another five years.

Looking at the short term—say, three to five years—I believe Rocket Lab could launch its own Earth-observation constellation. That seems achievable.

Over a ten-year period, Rocket Lab should undoubtedly aim to operate its own orbital data-center service.

What could Rocket Lab buy next?

Rocket Lab has already acquired Mynaric, adding laser terminals for high-bandwidth links between satellites.

The next logical gap is the other side of that network: space-to-Earth optical communications and optical ground infrastructure.

A future acquisition could add optical ground stations, atmospheric and cloud mitigation, network-routing software and hybrid laser/RF connectivity.

That would matter for defense networks, Earth observation and, eventually, space-based data centers. Rocket Lab would control the satellites, power systems, optical links, launch and ground connection.

Strategically, this is the missing capability I would watch.

My conclusion

Iridium’s existing constellation will not support Rocket Lab hypergrow by itself. I would be very surprised to see its business growing by more than 15-20% YoY over the next five years. Its existing business is profitable and defensible, but mostly mature. It will certainly strengthen Rocket Lab’s financial position by adding a meaningful, cash-generating revenue stream that could even make the company profitable as early as 2027, when Neutron CAPEX begins to slow down.

The acquisition works if Rocket Lab uses Iridium to become something much larger: an end-to-end prime contractor capable of building and operating complete defense and commercial space infrastructure.

In terms of a proprietary Rocket Lab constellation, beyond what Iridium already has in operation, I struggle to see anything generating meaningful revenue before five years from now.

That is the opportunity.

Rocket Lab is not simply buying a satellite operator. It is buying the final operating layer it needs to compete for the largest contracts in space.

If you want access to:

My portfolio

all my trades in real time

my price targets and how I calculate them

Business Ontology content

My price targets will be shared in the Telegram Group and explained on my Youtube channel.

I share my thoughts on X.

I have a position in Rocket Lab, and please note that:

I can be and will be (hopefully not often) WRONG. This is just my personal strategy—NOT FINANCIAL ADVICE. I don’t know your financial or life situation well enough to give any recommendations. Please do your own due diligence and research. Don’t be LAZY.

Be the architect of your own destiny.

Ciao

Lorenzo

As I was an engineer in this area - Irridum is 3 decades old technology that was a global failure for Motorolla. I'm pretty sure it's very constrained on what it's capable of doing. It lost for 1/2G cellular networks decades ago and has all possible cost and technology disadvantages compared to modern mobile IoT on 5G or free LoRA alternatives.

It has very narrow gov sector use case on where there's no cell network coverage.

Spectrum may be the only valuable asset there - all the rest is through away.