Rocket Lab infinite TAM

$RKLB Q4 2025 ER Update

The content of this analysis is for entertainment and informational purposes only and should not be considered financial or investment advice.

Most people still think Rocket Lab = “that small satellite launch company”.

That’s the mistake.

My core thesis on Rocket Lab hasn’t changed, but only reinforced: RKLB is building an end-to-end space company, and the total addressable market in front of them is not “launch”. It’s the full space value chain, and it keeps expanding as the world gets more tense and more digital.

In 2026 and beyond, two forces dominate everything:

AI

Space

And they are starting to reinforce each other. If you want a simple mental model: AI is the brain, space is the high ground. You don’t want your brain to depend on someone else’s high ground.

That’s why I say Rocket Lab is going after an “infinite TAM”. Because Space is infinite, if compared to earth.

Table of Contents

Q4 2025 Update

L2C take aways and performance

Business Ontology Framework by L2C

Business Ontology

4D Valuation Model

L2C portfolio strategy

Q4 2025 Update

The new arms race: not tanks, but tests and cadence

When geopolitics heats up, governments don’t buy ideas. They buy capability.

And capability is not a PowerPoint. It’s:

frequency (how often can you deliver)

reliability (does it work every time)

speed (can you do it now, not in 5 years)

Management has been very explicit on this point:

Faster and more frequent hypersonic testing is an urgent need and a national priority.

And they also framed the moat in plain English:

Rocket Lab is the only credible provider that has demonstrated the ability to deliver this capability right now, not years into the future… This kind of cadence and reliability positions us well for programs like Golden Dome.

Right after came the market proof: this week Rocket Lab signed a $190M contract for a block buy of 20 HASTE hypersonic test flights over the next four years — the single largest launch agreement in the company’s history.

In defense, cadence becomes a moat.

It’s like Amazon Prime in e-commerce. Everyone can build a website. The killer feature is the logistics machine that delivers fast, consistently, at scale.

In space/defense, Rocket Lab is trying to become that logistics machine.

Rocket Lab goes “prime”: the $816M proof point

One of the most important signals in the latest update is the Space Development Agency award.

SDA awarded Rocket Lab an $816 million contract to build an advanced constellation of 18 spacecraft, the largest single contract in the company’s history.

Why does “prime” matter?

Because being a prime means you’re not just a supplier. You’re the one accountable. You become part of the inner circle of who the government trusts to deliver critical systems.

Historically, that club was basically legacy aerospace. Slow, expensive, protected.

Now we’re watching the “defense prime” world changing, similar to how software ate the world:

Anduril in defense

Palantir in data

and Rocket Lab trying to do the same in space manufacturing + launch + payloads

And this is where vertical integration stops being a buzzword. They explicitly said:

It’s important to point out that the acquisition of Geost played a significant role in securing this award.

Vertical integration: the flywheel nobody can copy overnight

Rocket Lab’s strategy is simple and brutal:

build rockets

build spacecraft

build payloads

build the manufacturing engine to ship all of it

Most competitors are single-product companies.

Rocket Lab is building a system.

And systems compound.

A good analogy is Apple:

Hardware + software + supply chain

not because Apple likes complexity, but because control creates margin, speed, and quality

In defense/space, control is even more important because timelines and reliability are everything.

And there’s a “hidden” upside that many investors ignore: once you’re in the flow of these programs, you can capture value not only as a prime, but also as a merchant supplier. Management pointed at it: as a merchant supplier into other primes, there are “additional subsystem opportunities… that could add a total capture value to approximately $1 billion” across payloads, solar power, reaction wheels, star trackers, software, and more.

“Datacenters in space” sounds crazy, but if it happens...

Now the spicy part: space-based data centers.

At first glance it sounds like science fiction.

But the logic chain is not stupid:

AI demand explodes

data centers on Earth face limits (power, cooling, regulation, land, grid constraints)

in orbit you have cold environment + potentially massive solar power

Will this happen fast? I don’t know. Probably it will take 5 to 10 years.

But I like how Rocket Lab is positioning itself for that world without betting the company on a single moonshot.

For example, the solar piece is not a detail — it’s the bottleneck.

If you want to put serious compute in orbit, you need industrial power generation. And management basically said the same thing: if space-based data centers become real, “rapid market growth… will be hampered if traditional solar cells are the only option.”

That’s why I find Rocket Lab’s solar push so interesting. They are not just selling panels, they are trying to unlock the cost curve.

They introduced a space-optimized silicon solar array: silicon historically had “low radiation tolerance and very low life expectancy” in space, so it was not considered viable. Their claim is they solved that and can now deliver “a really low cost per watt at industrial scale,” enabling “gigawatt class power generation” and “kilometer size scale” systems.

And the hybrid approach (high-efficiency cells + silicon) is smart engineering: use premium cells when power density matters, use silicon when cost and scale matter, and mix them when you need to optimize the trade-off.

If “compute in orbit” ever becomes a real market, whoever controls power + thermal + manufacturing at scale wins. Solar is step one.

L2C take aways and performance

Rocket Lab is a manufacturing + execution + national security story, with optionality on the next wave (proliferated constellations, payload verticalization, maybe even compute-in-orbit).

Because the real product is not the rocket.

The real product is: delivery of critical capability, at scale, repeatedly.

And that’s an infinite TAM world.

Before the conclusion, it’s important to mention that Neutron’s first launch has been delayed to Q4 2026 due to an issue with its fuel tank. Compared to the original guidance from early 2025, Neutron is now running roughly one year late.

This can be read in two ways.

The bad news: delays push out revenue, slow down capability development, and give customers one more reason to stick with the incumbent.

The bullish interpretation: if Rocket Lab — the company that built, owns, and operates one of the most reliable small launch vehicles in the world — needs this much time to industrialize a bigger rocket, it’s reasonable to expect competitors will need even longer.

In other words: the difficulty of scaling up launch is exactly why the medium-lift market is likely to stay a duopoly (SpaceX + Rocket Lab) for long enough to let Rocket Lab compound into a much bigger company.

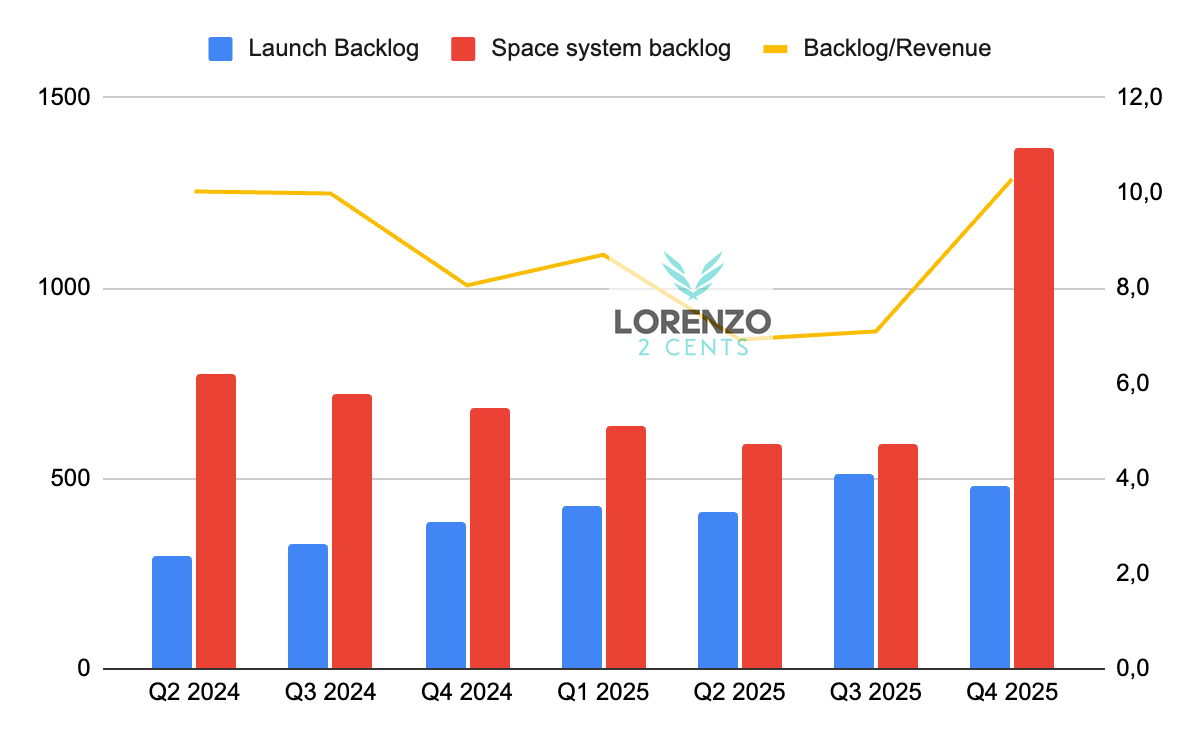

If you ask me what’s the best way to value Rocket Lab right now, I think it’s to monitor a simple ratio: Price-to-Backlog.

Backlog is not revenue, but in defense/space it’s the closest thing you get to forward visibility. And RKLB is increasingly behaving like a prime contractor, where the pipeline of awards matters as much as quarterly numbers.

Today, with backlog now above $2B, the Price-to-Backlog ratio is roughly ~20.

Here is how the backlog trend looked like in Q4 (You need to add the $190M of HASTE contract to get a more updated number).

My bet is that as Rocket Lab consolidates as a prime supplier, it will keep landing bigger and bigger contracts, and the backlog will stay full (or even expand).

As always, here is the “Deep Dive To Date” (DDTD), that is how the stock is performing since my initial deep dive. For RocketLab stock ($RKLB), the price on September 17th, 2024, when I published my analysis, was $7.19. As of this update, the price stands at $67, reflecting a

+9,3x DDTDFrom here on, the content is restricted to L2C Premium Members, folks who’ve chosen to unlock this toolkit and support my independent research:

Business Ontology Framework by L2C

Business Ontology: My core blueprint for modeling and tracking company performance at every level.

4D Valuation Model: the valuation tool I use to value all my investments (Fair price is useless)

L2C Portfolio Strategy: My portfolio allocation and strategy in details

L2C Portfolio access & trades alerts: Real-time views into my holdings, plus instant notifications on buys, sells, and shifts.

Business Ontology Framework by L2C

The Business Ontology is a framework I built after tearing apart several tech companies from the ground up—breaking them down to their basic parts and piecing together a real thesis on what drives them. Think of it as a map of a company’s soul. It’s a tight set of core indicators—tailored to each business—that show if it’s heading the right way, no matter what the stock price says. These aren’t your basic stats like P/E ratios or revenue bumps you grab from Yahoo Finance. They’re deeper, sharper, and linked straight to the thesis I’ve cooked up on how the company makes value and fights in its market.

The framework boils down to two big pieces:

The Business Ontology—This checks if the company’s worth buying into or hanging onto.

The 4D Valuation Model—This gives you a 4D roadmap to guide your own calls on how much to put in (allocation).

Now, let’s dive into Rocket Lab and this quarter’s update.

Business Ontology

Here’s a quick visual on the Business Ontology for Rocket Lab.