RocketLab: is future growth already priced in?

$RKLB Q1 2026 ER Update

Rocket Lab just reported another excellent quarter.

Demand is clearly not the problem.

Execution is not the problem.

The company is doing almost everything bulls wanted to see: revenue is growing, backlog is expanding, Electron is still proving its cadence, HASTE is becoming increasingly relevant for defense, and Neutron is attracting customers before its first launch.

On the business side, this was probably one of the strongest updates Rocket Lab has ever delivered.

But that is not the only question that matters for investors.

The real question is different:

How much of the future is already priced into the stock?

And after updating my model, my answer is less comfortable than it used to be.

Rocket Lab remains an exceptional company. I still think it is one of the most strategically important public companies in the space economy. But at the current valuation, the stock no longer looks like the obvious asymmetric setup it was before.

The company may execute beautifully.

The stock may still do well.

But the margin of safety is much thinner.

Q1 was a very strong quarter

Rocket Lab reported record Q1 2026 revenue of $200.3 million, up 63.5% year over year. GAAP gross margin reached a record 38.2%, and non-GAAP gross margin was 43.0%.

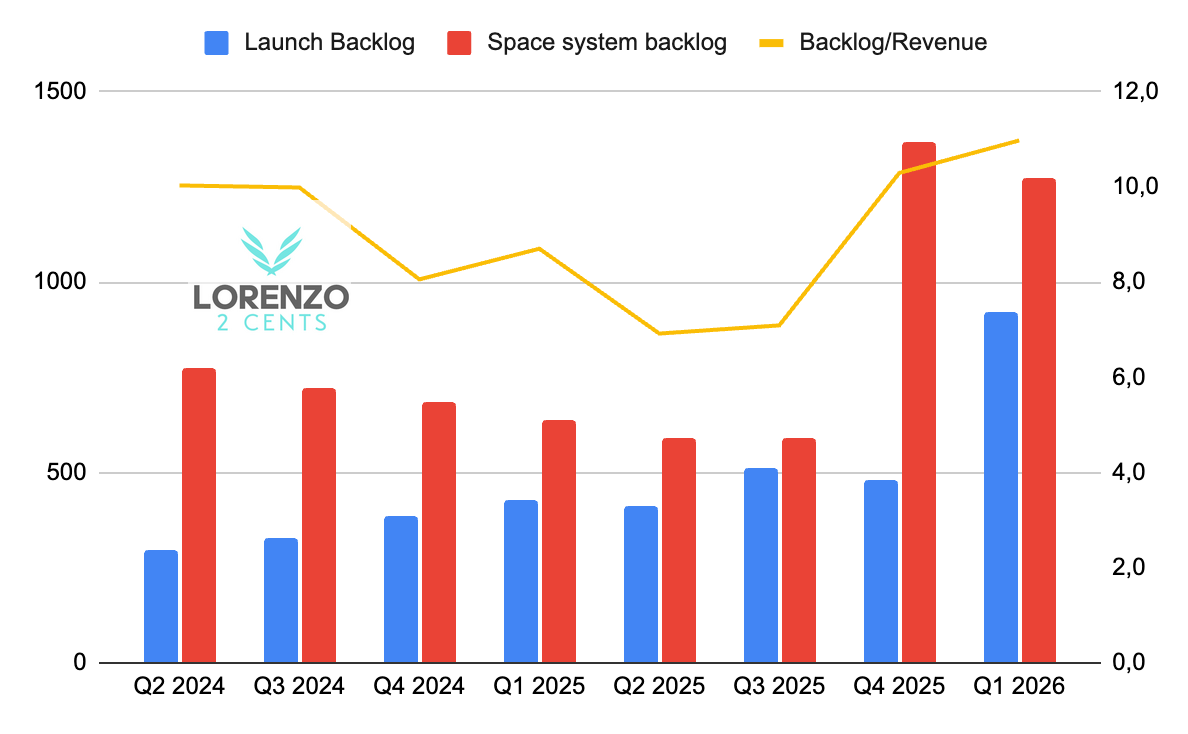

Backlog reached $2.2 billion, up 20.2% sequentially and more than double year over year.

That backlog number matters more than a normal quarterly revenue print, because Rocket Lab is not a simple transactional business. It is becoming a long-duration execution machine across launch, spacecraft, components, defense programs, and eventually Neutron.

Backlog is not revenue.

But in space and defense, backlog is the closest thing we get to forward visibility.

And the direction is very clear.

The backlog-to-revenue ratio increased sequentially again. Using Q1 revenue of $200.3 million and backlog of $2.2 billion, Rocket Lab is sitting at roughly 11x quarterly revenue in backlog.

That means demand is not just growing in absolute terms; the forward pipeline is growing faster than current recognized revenue.

That is exactly what you want to see from a company that is supposed to accelerate over time.

Peter Beck summarized the demand picture very well:

With the 31 Electron and HASTE launches and 5 Neutron contracts combined, we booked more launches in the first 3 months of 2026 than we did for all of last year.

That sentence is the bull case in one line.

Rocket Lab is not begging the market for demand.

The market is asking Rocket Lab for capacity.

Launch demand is inflecting

The most important signal in Q1 was not just revenue.

It was bookings.

Rocket Lab signed 31 new Electron and HASTE contracts in Q1, plus five dedicated Neutron launches.

This matters for two reasons.

First, Electron is still alive and very relevant.

Many people underestimate Electron because it is a small rocket, but that misses the point. Electron has cadence, reliability, and customer trust. In launch, those things matter more than PowerPoint capacity.

Second, Neutron is getting commercial validation before first flight.

That is important.

Neutron is still the biggest execution risk in the Rocket Lab story. Until it flies successfully, it is still a promise. But customers are already reserving capacity through the end of the decade, which tells you there is real market appetite for another reliable medium-lift provider.

The industry does not want only SpaceX.

Governments do not want only SpaceX.

Commercial constellation operators do not want only SpaceX.

The world needs more launch capacity, and it needs it from operators that can actually deliver.

That is where Rocket Lab has a shot.

Neutron still looks on track

The other key update is that Neutron is still expected to launch later this year.

No new delay was signaled in the Q1 update.

This is important because a large part of the Rocket Lab thesis now depends on Neutron. Electron is a great business, but it is not enough to justify the full long-term vision by itself. Space Systems is growing and becoming strategically important, but Neutron is what can turn Rocket Lab from a strong niche player into a true end-to-end space infrastructure company.

Neutron changes the size of the opportunity.

It opens the medium-lift market.

It gives Rocket Lab more control over its own space systems deployment.

It creates the platform that could eventually enable the services layer Peter Beck has talked about for years.

And that last point is key.

Because if Rocket Lab ever becomes more than launch + components + spacecraft manufacturing, if it eventually owns and operates services from space, the upside can be much larger than what a normal aerospace model captures.

But timing matters.

Peter Beck has been clear that services from space come after Neutron is established. That makes sense. You need the transportation layer before you can efficiently deploy and replenish your own infrastructure.

So even in an optimistic scenario, meaningful revenue from a services business is probably still three to five years away.

That does not mean it has no value.

The valuation is rich.

This is the uncomfortable part.

When I update my model, the conclusion is not that Rocket Lab is overhyped as a company.

The conclusion is that the stock price is already discounting a huge amount of success.

At the current valuation, the market is not pricing Rocket Lab like a speculative small launch company anymore. It is already pricing in a version of the future where:

Electron continues to grow and maintain strong cadence.

Space Systems compounds for many years.

Gross margins keep expanding.

Neutron launches successfully.

Neutron scales without major delays.

Rocket Lab captures a meaningful share of medium-lift demand.

Defense and national security demand remain strong.

The company keeps using its balance sheet well for M&A and vertical integration.

That is a lot of good news already embedded in the stock.

To be clear, none of these assumptions are crazy.

Actually, many of them are exactly what I want Rocket Lab to do.

The issue is not that the story is fake.

The issue is that the market now believes a large part of the story.

And when the market already believes, the asymmetry changes.

A year ago, the market was still treating Rocket Lab like a risky space stock with a small rocket and a dream.

Today, the market is closer to pricing it like a future space prime with a successful medium-lift rocket, a growing defense business, expanding margins, and long-duration backlog.

That is a very different setup.

What is not priced in?

In my view, the part that is not fully priced in — or at least not priced in enough — is the long-term services layer.

This is the part of the thesis where Rocket Lab stops being only a provider of launch and space systems, and starts monetizing infrastructure in orbit.

That could be constellations.

It could be data.

It could be communications.

It could be defense-related services.

It could be something we cannot precisely model yet.

This is why I have always liked Rocket Lab. Peter Beck is not building a small rocket company. He is building an end-to-end space company.

Launch is the access layer.

Space Systems is the manufacturing layer.

Services would be the monetization layer.

If Rocket Lab gets there, the upside can still be very significant.

But this is also the most uncertain part of the thesis.

It is far away.

It depends on Neutron.

It depends on execution.

L2C take aways and performance

Rocket Lab is still a great company. But the stock is no longer an obvious asymmetric bet at this valuation.

I remain invested.

But I am watching closely, and I am ready to take action if the risk/reward keeps deteriorating versus other opportunities in the portfolio.

I will soon publish a video where I explain my updated Rocket Lab 4D valuation model and the assumptions behind it.

If you want access to:

My portfolio

all my trades in real time

my price targets and how I calculate them

Business Ontology content

My price targets will be shared in the Telegram Group and explained on my Youtube channel.

I share my thoughts on X.

As always, here is the “Deep Dive To Date” (DDTD), that is how the stock is performing since my initial deep dive. For RocketLab stock ($RKLB), the price on September 17th, 2024, when I published my analysis, was $7.19. As of this update, the price stands at $102, reflecting a

+14x DDTDPlease note that:

I can be and will be (hopefully not often) WRONG. This is just my personal strategy—NOT FINANCIAL ADVICE. I don’t know your financial or life situation well enough to give any recommendations. Please do your own due diligence and research. Don’t be LAZY.

Be the architect of your own destiny.

Ciao

Lorenzo