$ZETA is the Marketing Vertical Ontology

ZETA Deep Dive - Part 2

AI is pushing the cost of making things down.

Writing copy gets cheaper.

Designing landing pages gets cheaper.

Building software gets cheaper.

Producing content (video, images, ads) gets cheaper.

Soon, with humanoid robots, even physical goods and services will get cheaper to produce and deliver.

When production becomes commoditized, differentiation shifts to distribution.

In practice, that means a higher % of enterprise revenue will go to:

demand generation

retention and lifecycle marketing

personalization and automation

measurement and attribution (or better: outcome-based ROI)

Marketing turns into the main “battlefield” because every product starts to look similar, faster.

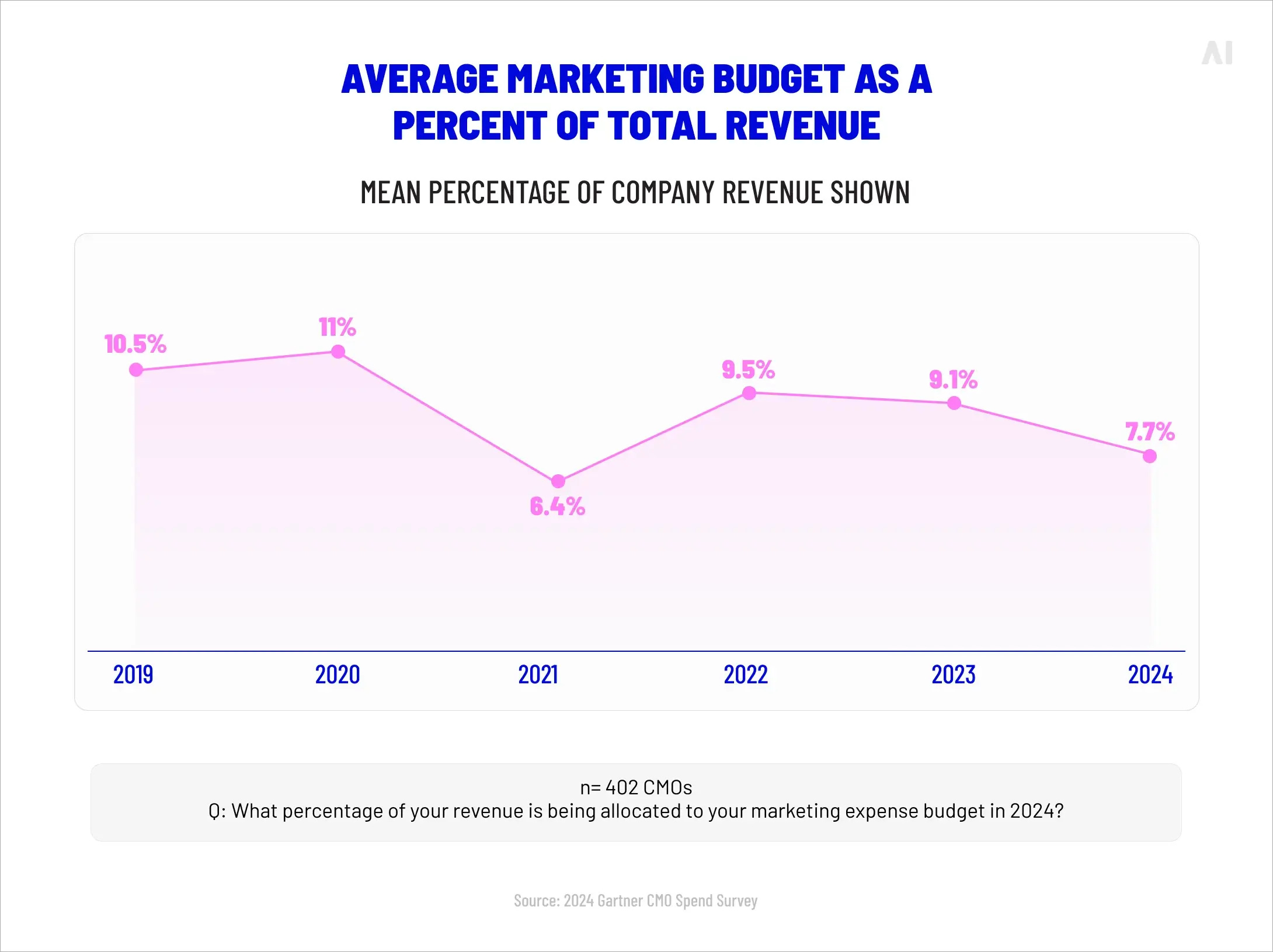

I bet that the following downtrend is going to reverse soon.

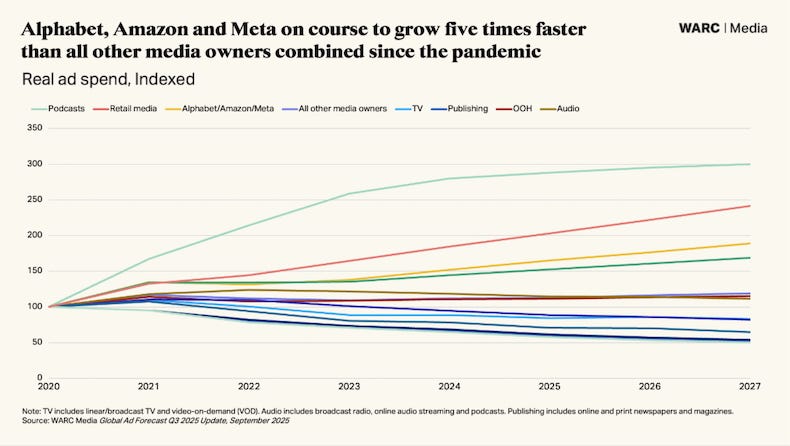

As the ad market consolidates into “walled gardens” (Meta, Google/YouTube, Amazon, TikTok), a larger share of every incremental marketing dollar gets spent inside closed ecosystems where the platform owns the identity, the inventory, and—crucially—the measurement.

In that world, the “tax” advertisers pay is not only higher CPMs; it’s also the inefficiency created by siloed data and last-click-style reporting. That’s where Zeta becomes a commission to pay on walled gardens: a layer that sits on top, resolves identity, and optimizes spend allocation based on outcomes—not on whatever each garden claims. Zeta’s data cloud is built around a durable person-level graph (hundreds of millions of opted-in people, with thousands of attributes per profile) and its first-party pixel footprint across massive web surfaces, which gives it an independent signal set to judge incrementality and ROI across channels.

The Meta partnership is a concrete example of why this matters: David Steinberg has said Zeta has “a matching between the Zeta ID and the Meta ID,” which lets Zeta connect exposures in Meta to downstream actions and then orchestrate the next best message/channel (e.g., follow with CTV, email, or another paid impression) based on the highest expected ROI. Put differently, if walled gardens are where the budget must live, Zeta is the vertical “marketing ontology” that makes that budget work harder—because it understands who the person is (identity), what to do next (propensity), and where to spend (allocation) in one closed-loop system.

If you have not read it, check my ZETA deep dive part 1:

If marketing is the battlefield, ROAS is the weapon

In a world where everyone can build, the winners are the companies that can sell.

For an enterprise buyer, the “best marketing cloud” is not the one with the most features. It’s the one that:

gets the highest ROAS (return on ad spend)

makes ROAS more predictable

scales ROAS across channels

proves it financially (CFO-grade reporting)

That’s why the category is structurally winner-takes-most.

If Vendor A gives you 2x ROAS vs Vendor B, you don’t “diversify vendors”. You reallocate budget.

In the last earnings call, David Steinberg (CEO) framed it very directly:

The marketing ecosystem grew about ~10%, while Zeta grew ~30% — and he explicitly said that this is Zeta “taking meaningful market share”.

On wallet share: he said Zeta’s 603 global enterprise clients spent about $100B in marketing last year and Zeta captured ~1.3% of that spend (~$1.3B revenue). (Math check: 1.3% × $100B = $1.3B.) He also shared a long-term goal of 10% wallet share.

Retention backs it up: net revenue retention hit a record 120% in 2025 (up from 114% in 2024).

He also explained the basic mechanism: “the higher we drive the return on investment, the greater the percentage of budget that our clients move to us.”

This is the “budget gravity” thesis:

deliver superior ROAS

get more wallet share

invest more in product + data

deliver even better ROAS

Flywheel.

Zeta is stealing share to Salesforce, for comparison.

If Zeta grows ~30% while the overall ecosystem grows ~10%, somebody has to be losing share.

Salesforce is a natural place to look because it’s one of the biggest incumbents in enterprise marketing.

One public data point that supports the narrative:

Salesforce’s Marketing + Commerce segment declined ~1% YoY in Q4 FY26 (constant currency), according to Salesforce’s quarterly breakdown.

Why I think Salesforce (and other incumbents) can’t easily “catch up”:

Legacy architecture + latency: many suites were assembled via acquisitions; stitching data + channels together often adds delay and complexity. In a ROAS world, milliseconds matter.

Different center of gravity: incumbents are optimized around being the system of record (CRM). Zeta is optimized around being the outcome engine (identity + activation + measurement). Those are different products, cultures, and data assumptions.

Signal disadvantage: Zeta’s data cloud/pixel footprint means more third-party-like signals feeding optimization loops. Incumbents can buy AI, but it’s harder to buy continuously-updating proprietary signals at that scale.

Enterprise switching dynamics: when a platform shows provably higher ROI, budgets migrate faster than core CRMs do — so challengers can win share even if the incumbent “stays installed”.

This is not “proof” by itself — but it’s exactly the type of footprint you expect when:

legacy stacks slow down

budgets get reallocated toward higher-ROI platforms

enterprises separate “CRM system of record” from “marketing outcome engine”

Zeta is trying to be that outcome engine.

The data moat is the product

Zeta’s moat is not “AI”. AI will commoditize.

Zeta’s moat is data + identity + signals at scale, and the ability to activate those signals across channels.

Steinberg gave the most important numbers in one quote:

“We have 552 million active people who are opted in our data cloud today with an average of 5,000 to 7,000 data elements per person. Our first-party tracking pixel sits on 1 trillion pages of content and ingest trillions and trillions of proprietary marketing signals…”

Those numbers matter because they describe:

scale (552M people)

depth (5k–7k data points per person)

freshness (signals ingesting continuously)

distribution surface (pixel on 1T pages)

That is the raw material to train models, build propensities, measure incrementality, and optimize campaigns in near real-time.

Why this matters now more than ever?

Steinberg also made an important observation about the current shift in traffic:

Google now answers 60%+ of queries on its own platform (down from the old world where “90%+” of queries were sent out to publishers).[1]

The conclusion is clear:

When “free clicks” disappear, marketing becomes harder and more expensive.

And when marketing becomes more expensive, the value of a platform that can:

find the right audience

personalize the message

measure outcomes

reallocate budget dynamically

…goes up.

The “ROAS compounding” piece: why Athena matters

Steinberg used an analogy I love:

Zeta built an “F-22 fighter jet”, but clients were flying it like a “Cessna”. Athena becomes the copilot that lets customers use more of the machine.

This matters because it points to a second order effect:

If Athena makes customers more effective, their ROAS goes up

If ROAS goes up, their budget moves to Zeta

If budget moves to Zeta, Zeta gets more signals

If Zeta gets more signals, the models get better

It’s not “AI feature”. It’s distribution + data + ROI loop.

Key risks

Regulation / privacy: Zeta’s advantage is signals + identity (including its pixel footprint). Any tightening around consent, tracking, data sharing, or cross-site identifiers could reduce signal quality or raise compliance cost.

Data-source scrutiny: even if data is “opt-in”, the market is increasingly skeptical about where signals come from and how durable the permissioning really is.

Steinberg reputation / past controversies: the CEO’s history (and periodic short-seller narratives) can raise the bar for trust and keep the valuation multiple suppressed even when fundamentals are strong.

My take

The Zeta thesis is not “marketing grows”.

It’s: marketing becomes the profit engine in a commoditized world.

And in that world, the company that can prove higher ROAS will win share, even against the biggest incumbents.

Zeta is explicitly telling you this is already happening — and the growth delta (30% vs ~10% ecosystem) plus the early cracks in legacy segments support it.

Potential catalysts from here:

Athena going GA (announced March 24, 2026) could increase adoption inside existing accounts and drive faster wallet-share expansion.

Next earnings is imminent (Q1 2026 on April 30, 2026). Any beat/raise + continued strong NRR can change the narrative quickly.

Dilution is coming down: dilution used to be much higher (~15% in FY2024), then management guided 4%–6% for FY2025 and is targeting 3%–4% net dilution in FY2026.

In the latest disclosures, management said they ended 2025 at the low end of their range with total net dilution of 4.3% (or 2.2% excluding Marigold) and improved stock-based comp from 19% of revenue in 2024 to 14% in 2025.

Valuation reset: the stock still trades like a “question mark”, not like a compounding 30% grower — which is exactly why the upside (and the risk) can be asymmetric.

Business Ontology Framework by L2C

The Business Ontology is a framework I built after tearing apart several tech companies from the ground up—breaking them down to their basic parts and piecing together a real thesis on what drives them. Think of it as a map of a company’s soul. It’s a tight set of core indicators—tailored to each business—that show if it’s heading the right way, no matter what the stock price says. These aren’t your basic stats like P/E ratios or revenue bumps you grab from Yahoo Finance. They’re deeper, sharper, and linked straight to the thesis I’ve cooked up on how the company makes value and fights in its market.

The framework boils down to two big pieces:

The Business Ontology—This checks if the company’s worth buying into or hanging onto.

The 4D Valuation Model—This gives you a 4D roadmap to guide your own calls on how much to put in (allocation).

Now, let’s dive into it.