Lemonade: the Vertical Ontology of Insurance

$LMND Q1 2026 Earnings Update

Models are moving fast, open models are getting better, and inference will keep getting cheaper over time. If every company can access good-enough intelligence, then intelligence itself becomes less scarce.

So what becomes scarce?

The domain map.

The workflow.

The data.

The ability to turn AI into action inside a specific industry.

That is what I call a vertical ontology.

$LMND is building it in insurance.

Customers, policies, claims, risk, fraud, pricing, and service interactions. Insurance is a perfect domain for an ontology because the business is basically a machine for pricing uncertainty. The better the object graph, the better the underwriting. The better the claims loop, the better the data. The better the data, the better the model.

That is the flywheel.

I have been very vocal about this, but let me say it again.

Lemonade is becoming a vertical ontology because it was built around the idea of becoming an autonomous organization. Its IT systems and business processes were designed for that from day 1. And it runs mostly a D2C model, which gives it direct access to first party customer data. That data, plugged into those systems, makes Lemonade a vertical ontology that keeps learning in a reinforcing cycle.

No incumbent will ever achieve it. I think it is almost impossible because of the innovator’s dilemma, which I have already explained multiple times.

Now, on to Q1 earnings, which were stellar. Probably the best in the company’s history.

Topline growth acceleration: At $1.33 billion, In Force Premium grew 32% – extending their streak of IFP growth rate acceleration to ten consecutive quarters.

Revenue grew faster still, by 71% to $258 million, reflecting the impact of recent reinsurance transition and higher premium retention.

Gross Profit: Increased 159% YoY to $100 million

Q4 2026 EBITDA positive guidance confirmed.

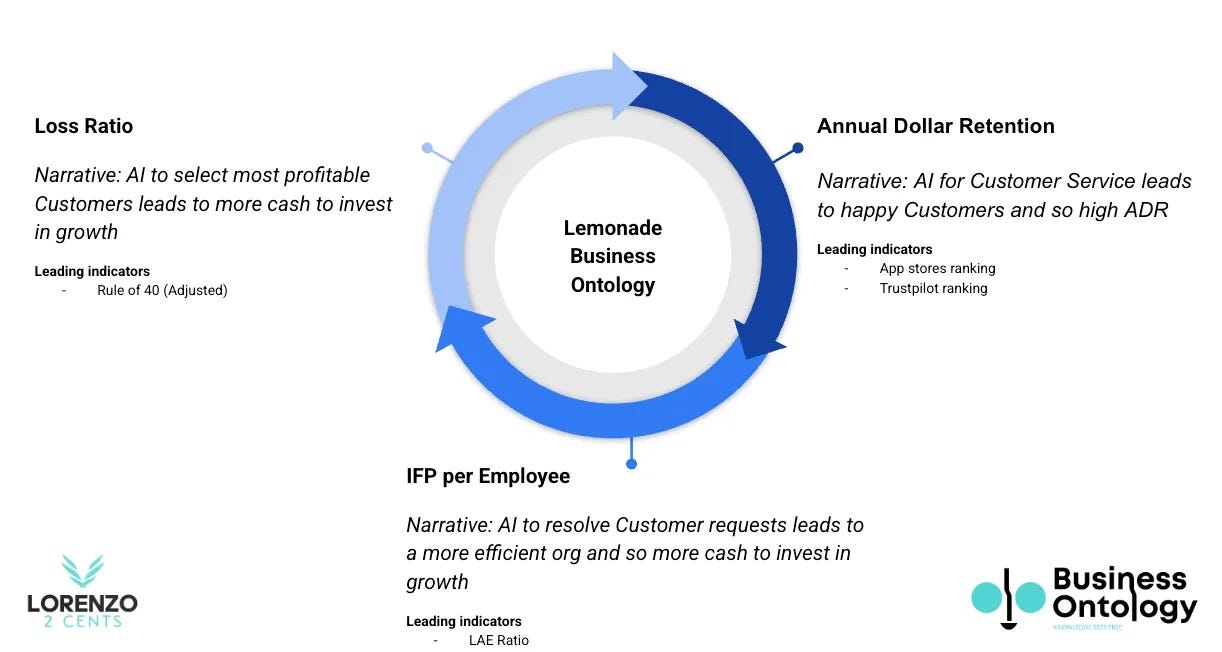

So it is time for an update of my Business Ontology for Lemonade. If you want to know more about what a business ontology is, let me know in the comments and I will write more about it.

Business Ontology Framework by L2C

The Business Ontology is a framework I built after tearing apart several tech companies from the ground up. I break them down to their basic parts, then piece together a real thesis on what drives them. Think of it as a map of a company’s soul. It is a tight set of core indicators, tailored to each business, that shows whether it is heading in the right direction, no matter what the stock price says. These are not basic stats like P/E ratios or revenue bumps you grab from Yahoo Finance. They are deeper, sharper, and linked directly to the thesis I have built on how the company creates value and competes in its market.

The framework boils down to two big pieces:

The Business Ontology—This checks whether the company is worth buying into (or holding).

The 4D Valuation Model—This gives you a 4D roadmap to guide your own decisions on how much to allocate.

Now, let’s dive into Lemonade and this quarter’s update.

Business Ontology

Here’s a quick visual on the Business Ontology for Lemonade.

Annual Dollar Retention

Annual Dollar Retention has been stable at 85% for a few quarters, after trending down from 88% in Q1 2024.

Management said the decline is primarily due to the continuing impact of their “clean the book efforts” in the home business. It should start rising again soon. There is no reason to doubt it after looking at the leading indicators:

App Store and Trustpilot rankings are above 4, which is extraordinarily strong compared to peers.

Happy Customers keep using the product.

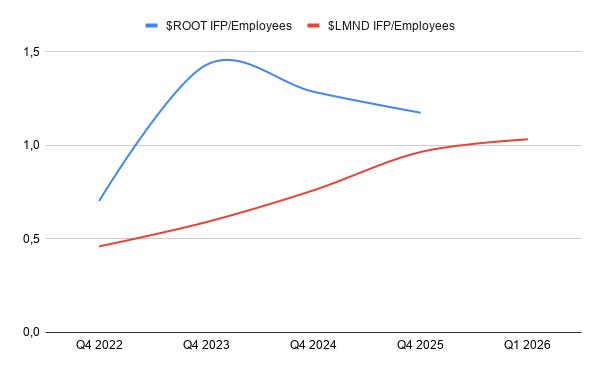

IFP Per Employee

IFP per Employee keeps rising and is about to overtake ROOT Insurance. For context,

Lemonade Premium per Customer is $424. ROOT Premium per Policy is $1423.

I could not find a perfectly comparable metric, but if you compare apples to apples the difference must be even more staggering (since a customer can have more policies).

The point is that ROOT should be much more efficient than Lemonade because any acquired or managed policy is worth on average 3 or 4 times more than Lemonade.

This is only a benchmark, but the takeaway is that Lemonade’s AI engine is firing on all cylinders, and my original thesis is slowly coming true.

The LAE ratio confirms the same point. At 6%, it is among the lowest in the industry.

Loss ratio

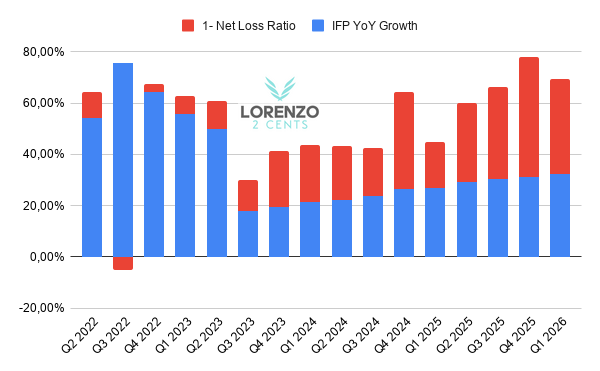

Loss ratio is at a healthy level: 62%. I do not expect it to go much lower than this, because Lemonade, as said multiple times, is optimizing the business to maximize gross profit, not to minimize loss ratio. The end goal is to make more money, not to have the lowest loss ratio in the industry.

To get a feel for how the company manages the trade-off between loss ratio and growth (lower loss ratio usually means higher prices, which usually means lower growth, and vice versa), let’s check my proprietary metric: Adjusted Rule of 40.

The higher, the better. Lemonade printed 69 in Q1, which is an excellent result that, if maintained, would drive outstanding gross profit growth.

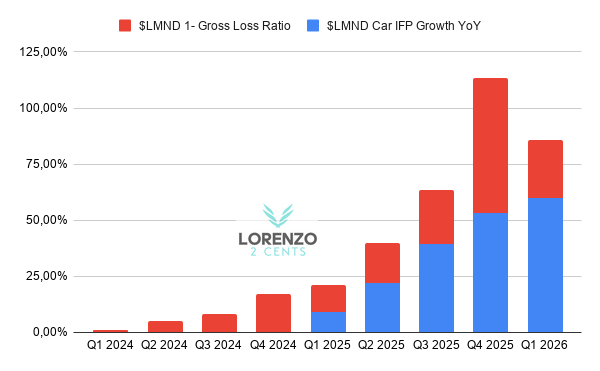

As management expects the car business to drive most growth in the near future, let’s see how the same metric is performing for the car segment.

The car business is growing healthy and strong, as shown by the positive trend in this metric. It prints even better than the overall business, even though it is not perfectly comparable. The car business is still tiny in absolute terms, so it benefits from “easy” hyper-growth that inflates the metric.

If you want access to the source of all the data I track, including what I used to update my business ontology, subscribe to Lorenzo2cents.

If you are already subscribed and you still do not have access to the Business Ontology Knowledge base, join the Business Ontology Community (Telegram channel) here.

4D Valuation Model

If you would like access to my 4D valuation model, including my price target, let me know in the comments of this post or in the Telegram channel. I will share it only if there is interest from enough people.

Lorenzo2cents (L2C) take aways and performance

My thesis on Lemonade—growth with near-zero marginal costs—is fully unfolding. As of now, there is not a single reason to doubt that 30% IFP growth for the foreseeable future, as guided by management, is achievable.

Even more, Lemonade is positioning itself to conquer a totally new market: autonomous agents and objects, which will be even bigger than the current insurance industry. If Lemonade captures a 5% market share of the US Property & Casualty (P&C), Auto Insurance, and autonomous objects market in 10 years, it will likely be a $1 trillion company.

As always, here is the “Deep Dive To Date” (DDTD), which shows how the stock is performing since my initial deep dive on September 24th 2024, when the stock price was $17.23.

3.3x DDTD

Lemonade (LMND) remains my highest-conviction holding and largest portfolio position.

Unlike other names (e.g., HIMS), Lemonade faces no acute, company-specific legal or regulatory headwinds that would derail its trajectory. Standard industry risks (e.g., compliance, reinsurance, AI model scrutiny) exist, but nothing idiosyncratic suggests near-term impairment.

The position is fully built. I have no plans to sell or add, except that I may use options or other trades to take advantage of market dislocations from real value, as I did in the recent drop. If you want to follow my moves in real time, join the Business Ontology Community on Telegram.

There you will also find the link to access my portfolio.

Here is an example of a message I sent on Monday, when I swapped my Meta shares for ZETA Global shares.

I expect Lemonade to be the primary driver of portfolio returns over the next 5+ years.

I can be and will be (hopefully not often) WRONG. This is just my personal strategy—NOT FINANCIAL ADVICE. I don’t know your financial or life situation well enough to give any recommendations. Please do your own due diligence and research. Don’t be LAZY.

Be the architect of your own destiny.

Ciao

Lorenzo