Rocket Lab: Just Exit Your Position, If in Doubt

$RKLB Q2 2025 ER Update

Since my last update on Rocket Lab in May 2025, where I highlighted how the investment in the company was tilting the asymmetry heavily to the upside, the stock has nearly doubled. Has the market finally caught on?

Maybe, but let's bring things back down to earth.

In this piece, I'll outline potential short-term headwinds while reaffirming the long-term thesis.

At its core, Rocket Lab's story remains a high-stakes bet on the space economy's explosion—or stagnation.

Rocket Lab's bullish case is straightforward: it's a call option on the space economy. If the sector booms, Rocket Lab could multiply in value alongside it. If it fizzles, the company might struggle to stay afloat amid heavy investments. This is because management is pursuing the entire supply chain, aiming to become a true end-to-end space company, as they've declared from the start.

Peter Beck, Founder and CEO, summed it up well during the Q2 2025 earnings call, speaking about the Vector Hays mission for the space force:

We're bringing the full stack of offerings across the satellite design, component manufacturing, integration and testing flight software, ground mission and launch licensing and the launch itself and on-orbit operations. We own the entire mission life cycle and its capability for national security that very, very few others can provide.

In the Q2 earnings release, Rocket Lab announced another key piece: the imminent acquisition of Geost, which bolsters their payload capabilities. Geost specializes in optical systems for missile warning, tracking, and space domain awareness—critical for government missions. As the company noted in their materials, this

Secures the domestic supply chain of this critical technology for next-generation missile defense initiatives, like the Golden Dome and the SDA constellations.

During the M&A call on May 27, 2025, Beck emphasized:

Adding payloads on top of launch and spacecraft really cements our status as a one-stop shop for national security.

The deal, valued at $275 million in cash and stock plus up to $50 million in earn-outs, is expected to close in the second half of 2025. It expands Rocket Lab's footprint to Tucson, Arizona, and northern Virginia.

Rocket Lab is emerging as the go-to choice for both governments and commercial clients. Their team executes reliably and on time, with expertise across the supply chain and top-tier integration.

They offer fast, reliable, affordable solutions under firm fixed pricing, with flight-proven tech and end-to-end execution. Why would anyone risk going elsewhere?

Beck reinforced this edge:

Our income in sensor payloads, for example, are also in play for an SDA award and through other bidders. We can control the cost and reduce the schedule risk through our vertical integration in a way that others can't. And we hold the keys to their technology and components that are foundational to these contracts.

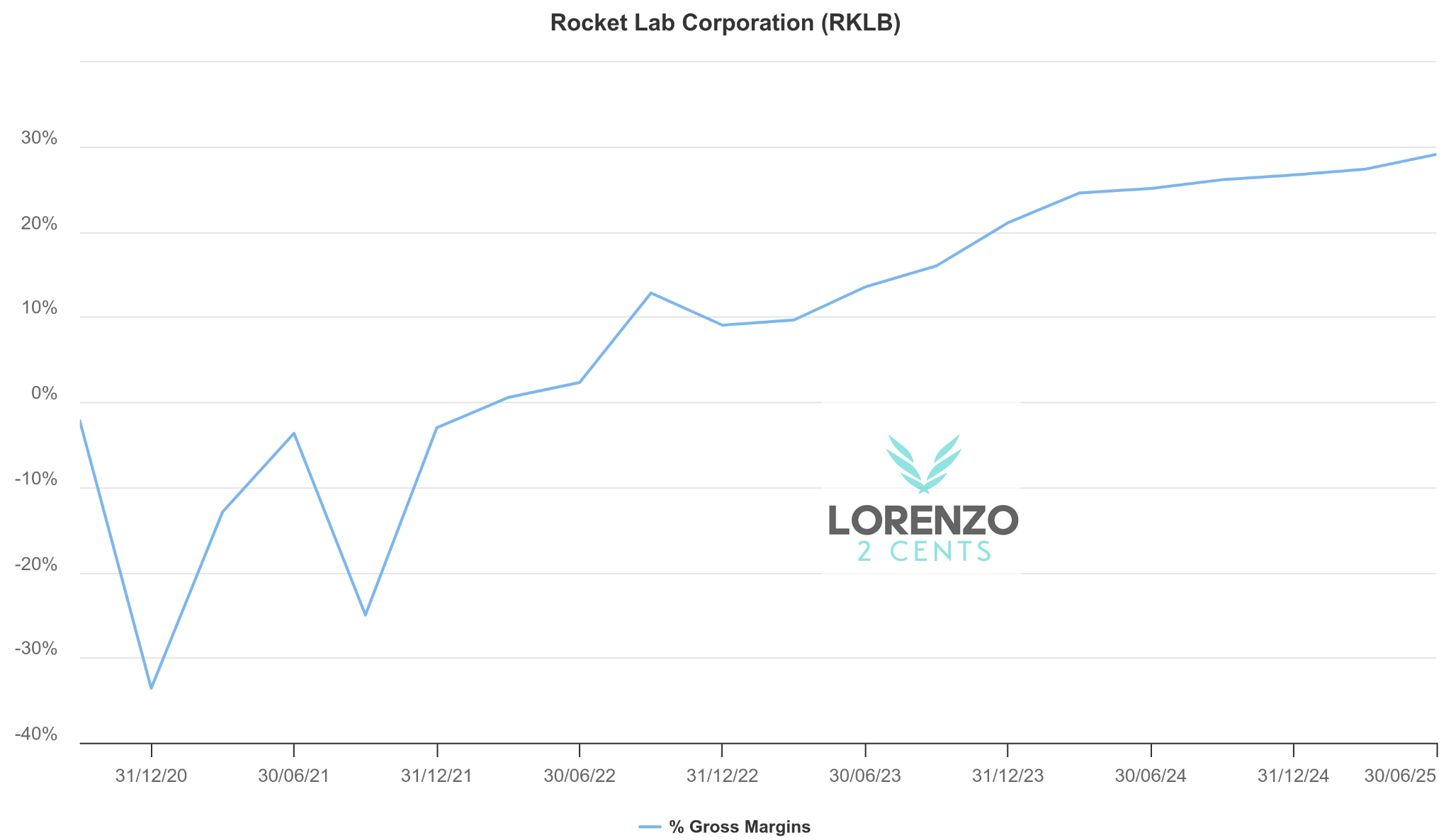

In Space Systems, prime contractor status is growing, with the ability to build and deploy entire satellite systems aligning perfectly with U.S. defense strategy. As capabilities expand—organically and through acquisitions like Geost—margins improve, and the moat widens.

Competitors might charge more while covering less ground.

No further proof needed that management can handle this complexity—they've already proven it.

Electron hit a milestone:

Four of the quarter's five missions took place within four weeks - proving our capability to conduct weekly launches.

Backlog and orders tell the story; if customers trust Beck, so do I.

Electron selected to launch dedicated mission for the European Space Agency for the first time. Launch scheduled from Launch Complex 1 in Q4 2025.

Electron is nearing profitability at scale, and the playbook will apply to Neutron. Space Systems likely sustains itself already.

Rocket Lab is approaching escape velocity, making it hard for others to catch up. New players might emerge in niches, but few will match the end-to-end scope, positioning Rocket Lab as a key gatekeeper.

Thus, the thesis hinges on one question: Will the space economy boom? If yes, Rocket Lab grows exponentially. If not, survival gets tough given their pace of investments.

Paper Hands Should Exit Now (No Financial Advice)

I'm seeing more chatter on Fin-X about Rocket Lab's high multiples— are they justified? What's the remaining upside? Time to sell?

If you're pondering these, consider exiting. A perfect storm could hit in the next three months, potentially dropping the stock 50% or more.

First headwind: Backlog/Revenue has declined for over a year.

Launch backlog grows steadily, but Space Systems' is shrinking, more than offsetting it.

This signals less contract value on hand for future revenue.

Sequential rebalancing in backlog mix as healthy Launch bookings continue, offset by another strong quarter of Space Systems revenue recognition.

Essentially, they're recognizing Space Systems revenue faster—positive for execution and cash flow.

CFO Adam Spice explained:

Space Systems bookings remain lumpy given the timing of increasingly larger needle-moving customer and program opportunities but remains at a healthy level despite a step-up in revenue run rate for the past few quarters.

And:

We continue to cultivate a healthy pipeline in multi-launch deals and large satellite manufacturing contracts that, as mentioned earlier, can create lumpiness in backlog growth, given the size and complexity of these opportunities.

Management attributes the drop to bigger, lumpier deals with shorter delivery times, allowing revenue growth even with lower backlog. Beck added:

Our advantage is our commercial speed improving execution. The way programs like this have been built in the past, dominated by the large defense primes just won't work the same time -- this time around to meet the administration's urgent time line. And this agility and innovation, vertical integration and on-time delivery and execution. That's why we've delivered time and time again across our programs to date and what we stand ready to deliver for the Golden Dome.

I buy it—it's reflected in the guidance:

Expect revenue to range between $145 million to $155 million,

a minimum 38% YoY growth, accelerating from Q2's 36%.

Expect year-on-year increases in both Space Systems and Launch revenue.

But lumpiness means I wouldn't be shocked by a guidance miss in the next couple of quarters. It's the Rocket Lab business's nature. It can happen. It will happen. Are you ready?

Second risk: Neutron delay or first launch failure. Highly likely. Communication has shifted subtly. Peter Beck:

There are still some risks to retire like propulsion and full integration of Stage 1 testing, which we're taking our time on to make sure we're successful

And:

All in all, we continue to push extremely hard for an end of year launch. We're continuing to run a green light schedule with Neutron, which means every single thing needs to go to plan that they're scheduled to hold, but I also want to stress that we're not going to rush and take stupid risks to get a launch Neutron before it's ready. In the context of the life cycle of the vehicle and the program a couple of months here or there is completely irrelevant. What's really important is performance, reliability, scalability right from the get-go, and there'll be no cutting corners here to just rush to the pad for an arbitral deadline.

Conclusion

Everything's on track; RKLB 0.00%↑ advances at full speed, and the future looks incredibly bright as they solidify their position as a leader in the space race. The end-to-end build progresses well. Spice:

We exited Q2 in a strong position to execute on our organic expansion opportunities as well as inorganic options to further vertically integrate our supply chain and grow our strategic capabilities and expand our addressable market consistent with what we have done successfully in the past.

Long-term, the thesis holds stronger than ever—get ready for Neutron liftoff, together with Rocket Lab market cap! Short-term volatility? Be ready for it—or exit if in doubt. Only real long-term investors deserve to ride the Rocket Lab’s rocket.

As always, here is the “Deep Dive To Date” (DDTD), that is how the stock is performing since my initial deep dive. For RocketLab stock ($RKLB), the price on September 17th, 2024, when I published my analysis, was $7.19. As of this update, the price stands at $48.6, reflecting a

+6,7x DDTDStay tuned for the next update!

The content of this analysis is for entertainment and informational purposes only and should not be considered financial or investment advice. Please conduct your own thorough research and due diligence before making any investment decisions and consult with a professional if needed.